Health Care

There is substantial agreement that the US healthcare system has serious problems. A remarkably high 18% of GDP is devoted to healthcare—far higher than other developed countries, but without producing better health outcomes. Currently, 27 million people do not have health insurance—also a much higher rate than other developed countries.

Numerous proposals have been put forward in Congress and the White House to reduce the cost of healthcare—including the price of drugs which are substantially higher in the US than other developed nations—and reduce the cost of health insurance.

|

REDUCING HEALTHCARE COSTS |

|

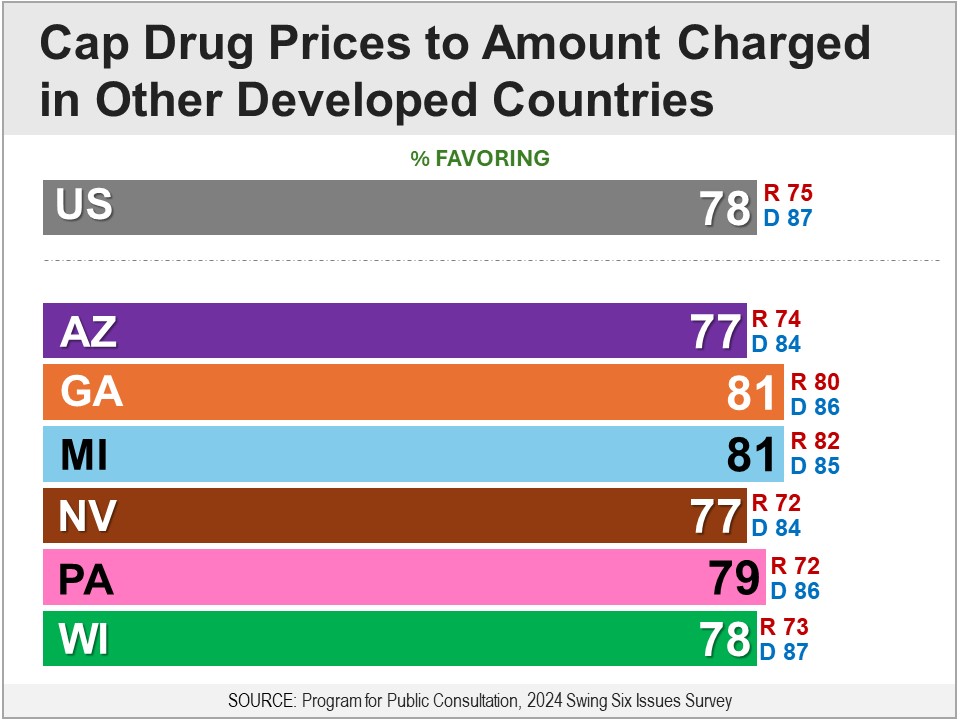

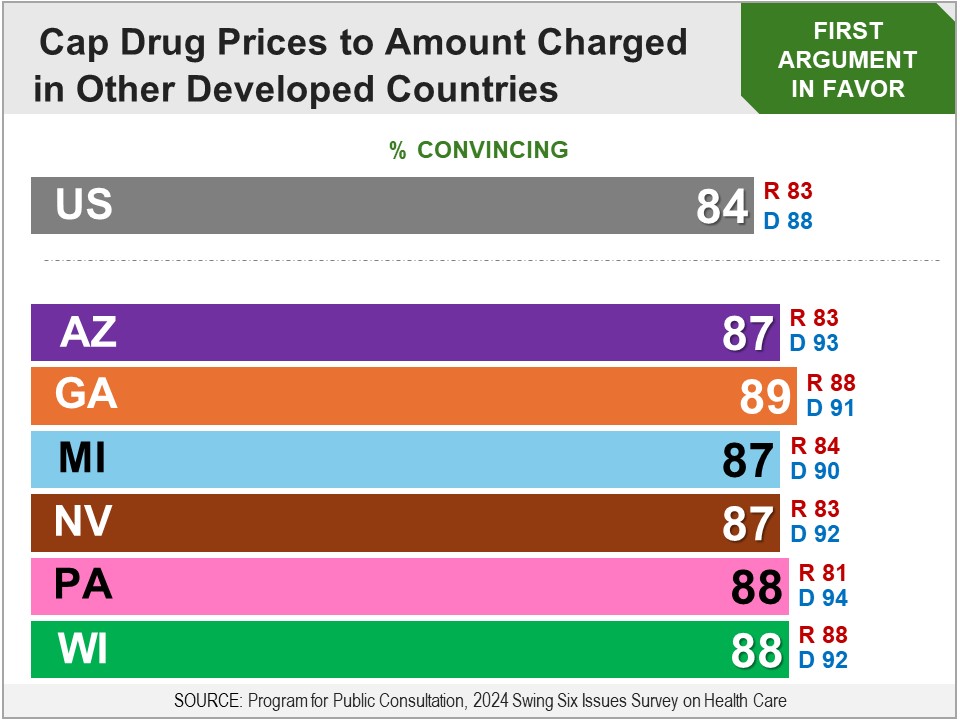

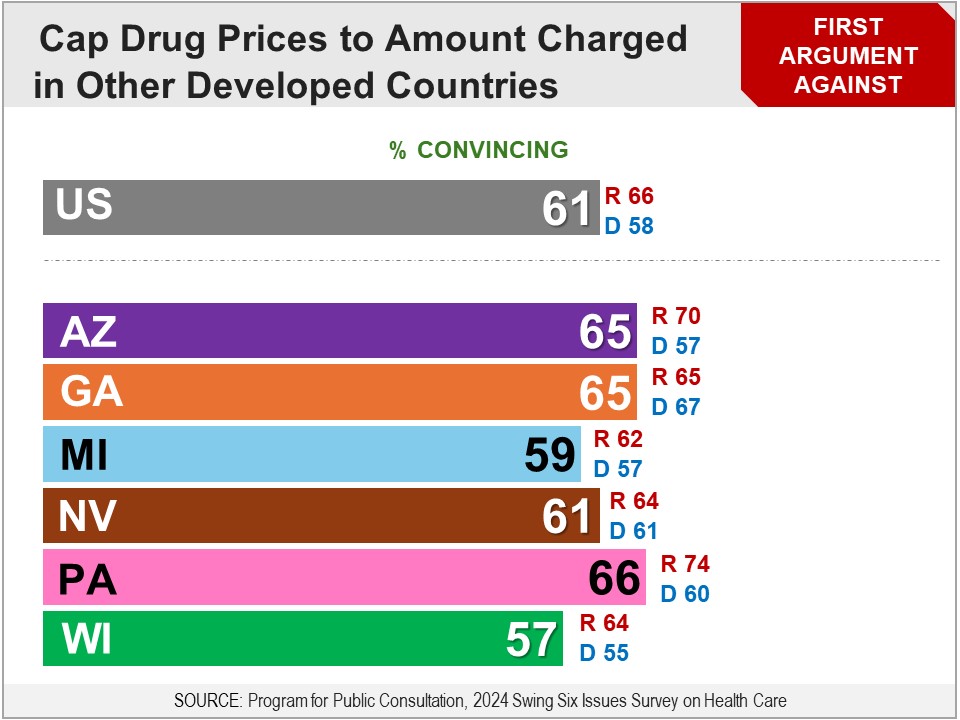

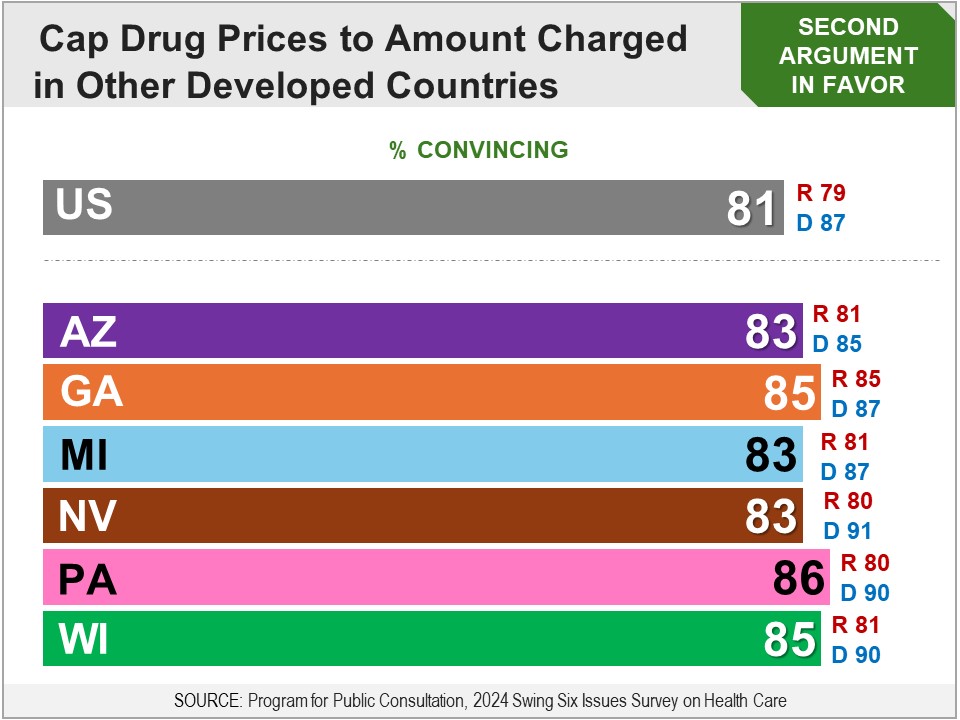

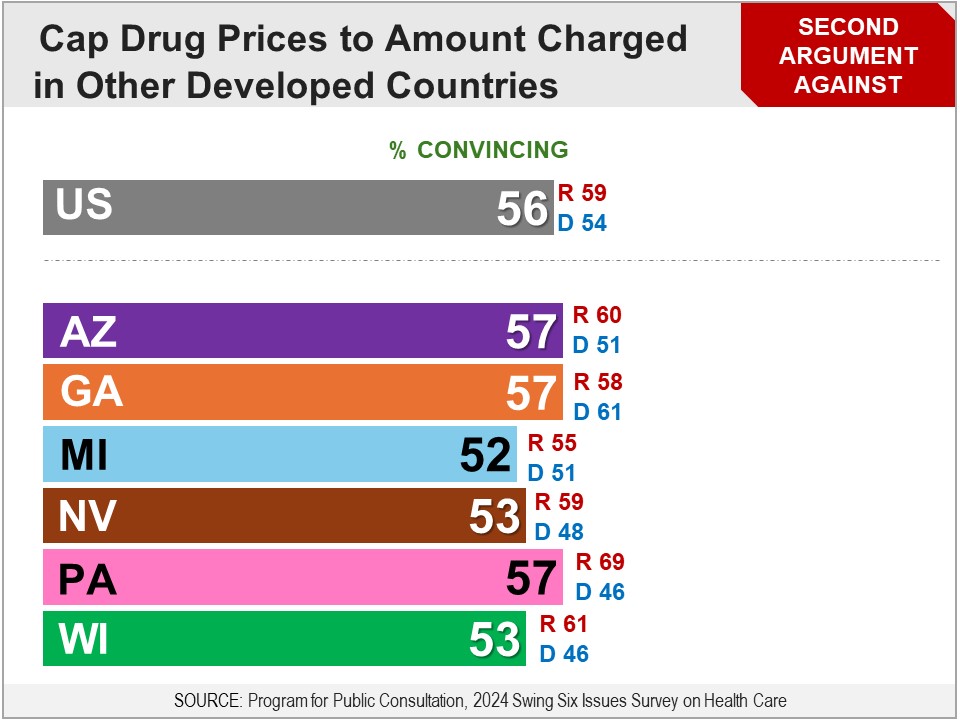

Survey: PPC, July 2024 Respondents were asked whether they favor the following proposal: The federal government shall set maximum prices that drug companies can charge for each prescription drug, based on what is charged for those drugs in other developed countries (such as Canada, Australia, Japan and many European countries). They had been informed in the briefing (see below) that prescription drugs in other developed countries are about half the price they are in the US. Asked for their final recommendation, a bipartisan majority of 78% were in favor, including 75% of Republicans, 87% of Democrats, and 67% of independents.

More Details Briefing Respondents were presented a briefing on the increasing price of healthcare, including the fact that spending on healthcare is much higher in the US than in other developed countries. They were then presented a briefing on the increasing price of prescription drugs: As you may know, the cost of drugs plays an important role in determining the cost of healthcare for all healthcare consumers, including those with insurance. Drug prices affect what people pay out-of-pocket for drugs, like for copays or coinsurance, and even more if the drug is not covered by their insurance. In 2021, twenty one percent of people reported that they did not get a prescribed drug because they could not afford it. Twelve percent reported taking less than the prescribed amount to save money. Something that impacts an even larger number of people is that the price of drugs affects the cost of health insurance premiums as health insurance companies pass the cost of drugs on to consumers. So, policies that reduce the cost of drugs will also reduce what people pay for premiums. Before looking at specific proposals, they were informed: As you may know, the prices that drugs sell for in other developed countries are on average less than half the price that Americans pay. They were then introduced to the first proposal: The federal government shall set maximum prices that drug companies can charge for each prescription drug, based on what is charged for those drugs in other developed countries (including Canada, Australia, Japan and many European countries). Drug prices are lower in other countries because nearly all health insurance is regulated by the government, and they set or negotiate prices for all drugs covered by insurance. However, in some cases, if a drug is determined to be too expensive, then it will not be covered by insurance in these countries. Drug companies are able to sell their drugs for less in other developed countries, while still making a profit, because the cost of manufacturing drugs is often very low. The larger cost for drug companies is the research and trials that are required to develop new drugs. Drug companies are opposed to the US government setting limits on how much they can charge in the US, saying that if they are required to lower the prices they charge in the US, this will: reduce the amount of revenue they have to invest in drug development, and reduce their ability to make profits so much that they will be less ready to take the risk of developing new drugs. The Congressional Budget Office has studied this issue and concluded that, if the government limits what drug companies can charge, the number of new drugs developed could be reduced by a few percent, but there is some controversy about this assessment. Arguments Respondents evaluated arguments for and against the proposal for, “the government to limit what drug companies can charge, to no more than what is charged in other developed countries.” The arguments in favor were found convincing by very large bipartisan majorities of over eight-in-ten. The arguments against did not do as well, but were still found convincing by bipartisan majorities of about six-in-ten.

Final Recommendation Respondents were presented a summarized version of the proposal: The federal government shall set maximum prices that drug companies can charge for each prescription drug, based on what is charged for those drugs in other developed countries (such as Canada, Australia, Japan and many European countries). Asked for their final recommendation, a bipartisan majority of 78% were in favor, including 75% of Republicans, 87% of Democrats, and 67% of independents.

Results in Six Swing States The survey was also fielded in six swing states: AZ, GA, MI, NV, PA and WI. Across all swing states, the proposal was favored by bipartisan majorities of 77-81%, including 72-82% of Republicans and 84-87% of Democrats. Capping Prices Only For Drugs Developed with Federal Aid After evaluating the proposal to cap the price of all drugs to what is charged in other developed countries, including the arguments for and against, they were presented a more limited proposal: The federal government shall set maximum prices that drug companies can charge for each prescription drug that is developed directly from research funded by the federal government, based on what is charged for those drugs in other developed countries. A bipartisan majority of 65% were in favor, including 62% of Republicans and 69% of Democrats. Preferred Policy After evaluating the proposals to cap the price of all drugs, and cap the price of drugs developed with federal aid, they were asked which they would prefer, or if they do not want either. A bipartisan majority of 58% preferred capping the price of all drugs, including 55% of Republicans and 66% of Democrats. Capping the price of only drugs developed with federal aid was preferred by 30% (Republicans 32%, Democrats 26%). Neither proposal was chosen by just 12%. Related Standard Polls A large bipartisan majority has favored letting the government negotiate drug prices so American consumers pay no more than other developed countries:

|

|

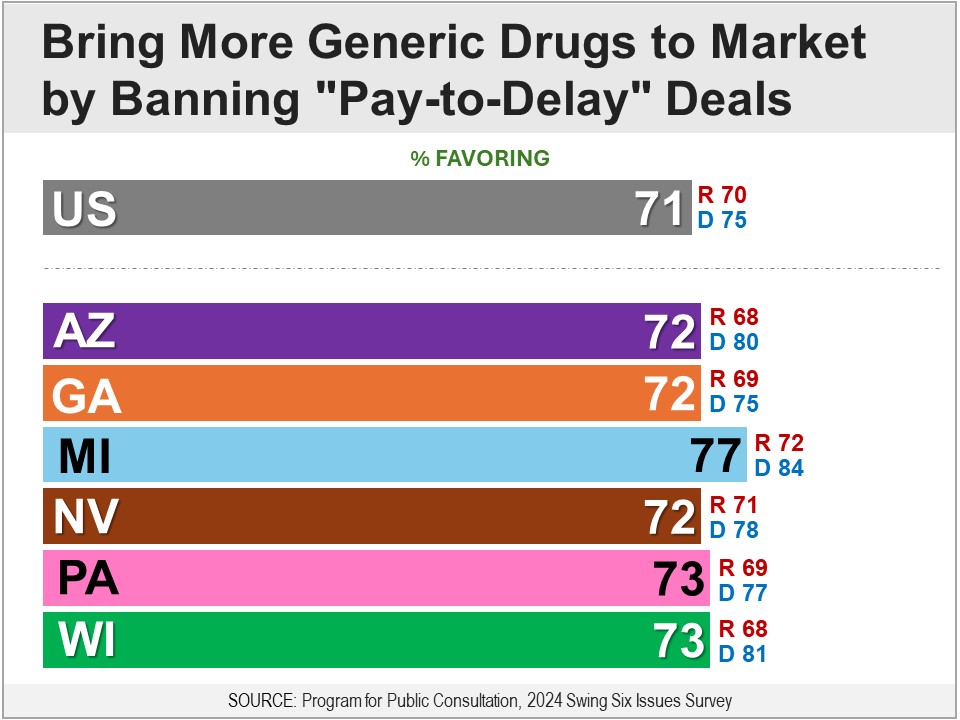

Survey: PPC, July 2024 Respondents were asked whether they favor the following proposal: When a drug company’s patent is about to expire, make it illegal for that drug company to pay generic drug companies to hold off on making and selling that drug. A bipartisan majority of 71% were in favor, including 70% of Republicans and 75% of Democrats.

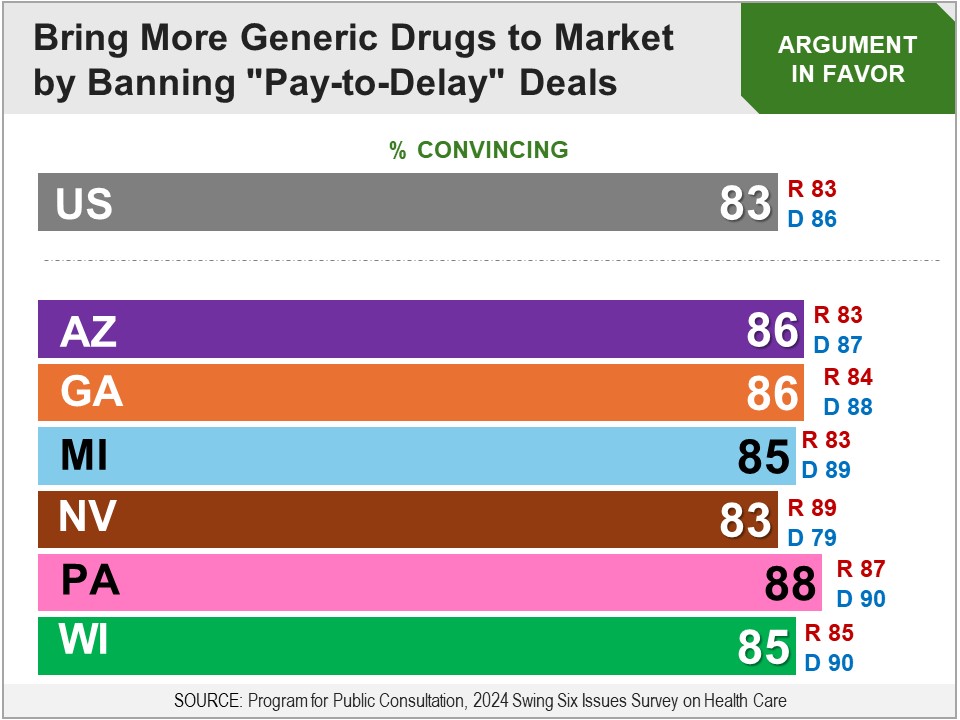

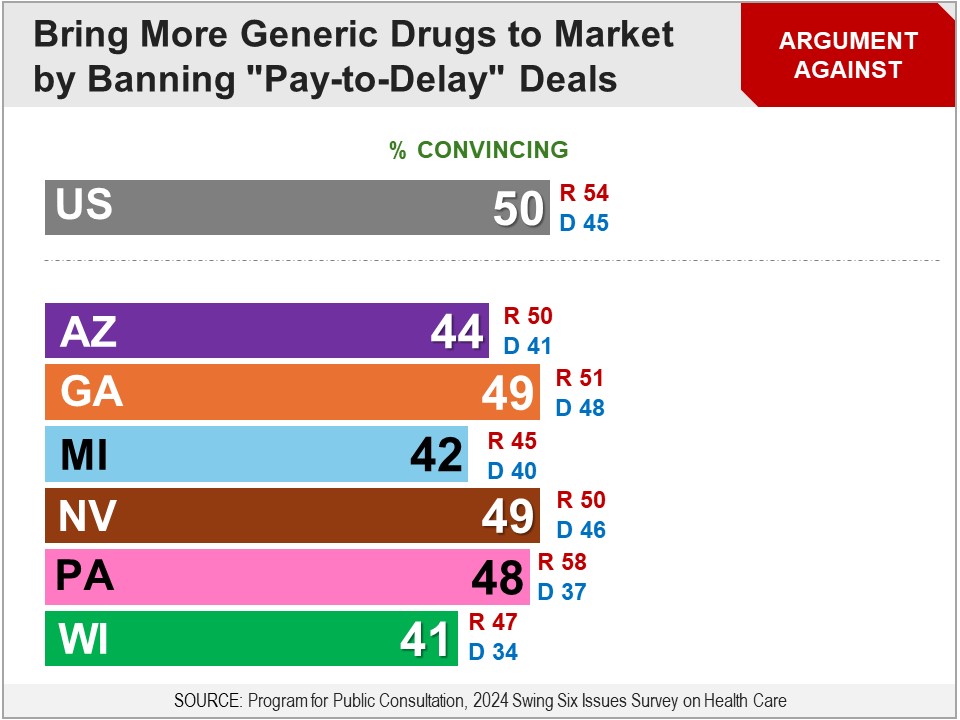

More Details Briefing Respondents were presented a briefing on prescription drug patents: Something that affects the amount of competition is patents on drugs. Here is what patents are: When a company develops a new product, such as a new drug, they can get a patent from the federal government. In that case, other companies are legally prohibited from making that product for several years. For drugs, it is for up to 20 years. Because there is no competition during those first years, the company with the patent can charge a price that is higher than if they had competition. The idea behind patents is that the drug company should be given enough time to sell the product without competition, so they can cover the costs of developing that product and make some profits. Once the patent expires, other drug manufacturers can start making that drug, such as “generic” drug companies which charge lower prices. This increases competition and prices come down. They were then introduced to “pay-to-delay” agreements between brand-name and generic drug companies: Some drug companies have been extending the amount of time their drug has no competition, after their patent expires. Here is one way they do this: When the patent on their drug is about to expire, and a generic drug company wants to start making that drug, the drug company pays the generic drug maker to hold off on making and selling that drug for a period of time, so that it can continue to charge the higher price without competition. In 2000, courts ruled that these deals violated anti-competition laws and were banned. Then in 2005, courts over-ruled that decision and allowed drug companies to start making these deals again. Since then, the number of these agreements has continued to increase. Respondents were told: A proposal has been put forward to pass a law that would make these deals illegal. Arguments The argument in favor was found convincing by an overwhelming bipartisan majority of over eight-in-ten, with little difference between Republicans and Democrats. The argument against did quite poorly, with just half finding it convincing, including less than half of Democrats and only a small majority of Republicans.

Final Recommendation Respondents were finally asked whether they favor the following proposal: When a drug company’s patent is about to expire, make it illegal for that drug company to pay generic drug companies to hold off on making and selling that drug. A bipartisan majority of 71% were in favor, including 70% of Republicans and 75% of Democrats.

Results in Six Swing States The survey was also fielded in six swing states: AZ, GA, MI, NV, PA and WI. Across all swing states, the proposal was favored by bipartisan majorities of 72-77%, including 68-72% of Republicans and 75-84% of Democrats. Results from Deliberative Democracy Lab In an in-person deliberation by Stanford University’s Center for Deliberative Democracy in September 2019, respondents were presented with the following proposal: The US government should change the patent system so generic drugs are more quickly introduced into the marketplace. After receiving the briefing material, respondents deliberated on the proposal in-person. Finally, they were asked for their final recommendation. On a 0-10 scale, with 5 being “in the middle”, 88% favored (6-10) the proposal, including 81% of Republicans and 92% of Democrats. Status of Legislation Several pieces of legislation were introduced or reintroduced in the 118th Congress that would prohibit “pay-to-delay” deals:

None of these bills made it out of committee. |

|

Survey: PPC, July 2024 Respondents were asked whether they favor the following proposal: In the event the government determines the price of a patented drug is unaffordable to some or most of the people that need it, and that drug was developed with the aid of federal funding, the federal government will override the drug company’s patent and license other companies to produce the drug. A bipartisan majority of 73% were in favor, including 72% of Republicans and 79% of Democrats.

More Details Briefing Respondents were presented a briefing on the view that the President has authority to revoke patents for certain drugs developed with Federal aid, if they are too expensive for most who need them: Another proposal has been put forward to lower the price of some very high-priced drugs by increasing the amount of competition in the drug market. As mentioned, drug patents are issued by the federal government that allow a company to be the sole producer of the drug for 20 years. Under federal law it also has the authority to override patents on drugs developed with the aid of federal funds, under certain circumstances, and allow other selected companies to produce the product. One of these circumstances is if the patent is causing a product, which is necessary for public health or safety, to be inaccessible for a significant number of people who need it. However, this has never been invoked for drug patents. As you may know, there have been some cases in which the price of some new drugs has been so high that some insurance companies have refused to cover them. This happens in other developed countries as well. They were then told about the following proposal: This has led the government to consider invoking its power to override certain drug patents, as follows: In the event that the government determines the price of a patented drug is not accessible to some or most of the people that need it, and that drug was developed with the aid of federal funding and is necessary for public health and safety, the federal government will override the drug company’s patent, and license other companies to produce the drug as well. Arguments The argument in favor was found convincing by an overwhelming bipartisan majority of eight-in-ten, with little difference between Republicans and Democrats. The argument against did not do nearly as well, with just over half finding it convincing, including just over half of both Republicans and Democrats.

Final Recommendation Respondents were finally asked whether they favor the following proposal: In the event the government determines the price of a patented drug is unaffordable to some or most of the people that need it, and that drug was developed with the aid of federal funding, the federal government will override the drug company’s patent and license other companies to produce the drug. A bipartisan majority of 73% were in favor, including 72% of Republicans and 79% of Democrats.

Results in Six Swing States The survey was also fielded in six swing states: AZ, GA, MI, NV, PA and WI. Across all swing states, the proposal was favored by bipartisan majorities of 74-77%, including 70-75% of Republicans and 79-84% of Democrats. Results from Deliberative Democracy Lab In an in-person deliberation by Stanford University’s Center for Deliberative Democracy in September 2019, respondents were presented with the following proposal: The US government should change the patent system so generic drugs are more quickly introduced into the marketplace. After receiving the briefing material, respondents deliberated on the proposal in-person. Finally, they were asked for their final recommendation. On a 0-10 scale, with 5 being “in the middle”, 88% favored (6-10) the proposal, including 81% of Republicans and 92% of Democrats. Status of Proposal The proposal was put forward by the Biden Administration in 2023: Biden-Harris Administration Announces New Actions to Lower Health Care and Prescription Drug Costs by Promoting Competition. |

|

Survey: PPC, July 2024 Respondents were asked whether they favor the following: Congress passing a law to make permanent the policies that require hospitals and other health centers, and insurance plans, to make public the costs of healthcare services and products. A bipartisan majority of 77% were in favor, including 78% of Republicans and 82% of Democrats.

More Details Briefing Respondents were presented a briefing on price transparency: One factor that can affect the price of healthcare is whether people know the cost of the healthcare they need or want before they get it. It is often difficult for many people to find out the price that they will pay for a healthcare treatment or prescription before they decide to get it. Some experts believe that if these prices were made more available to the public – known as price transparency – it could lower prices for, and spending on, healthcare. Here is how they say this works:

They were then informed about Federal policies that have been in place since 2020 to require more price transparency: Since 2020, the White House – under both Presidents Trump and Biden – has put in place price transparency policies that require healthcare providers and insurance plans to publish the costs of most healthcare services and products. However, because these policies were put in place by the White House, they can be overturned by a future President. They were then told there is a proposal to make those policies permanent. Arguments The arguments in favor did very well, with overwhelming bipartisan majorities of around eight-in-ten finding them convincing. The arguments against did not do nearly as well – with one found convincing by just over half – but bipartisan majorities still found both convincing.

Final Recommendation Respondents were asked for their final recommendation on the following proposal: Congress passing a law to make permanent the policies that require hospitals and other health centers, and insurance plans, to make public the costs of healthcare services and products. A bipartisan majority of 77% were in favor, including 78% of Republicans and 82% of Democrats.

Results in Six Swing States The survey was also fielded in six swing states: AZ, GA, MI, NV, PA and WI. Across all swing states, the proposal was favored by bipartisan majorities of 75-84%, including 74-80% of Republicans and 76-88% of Democrats. Status of Proposal In the 118th Congress, a proposal to make that policy permanent was in several pieces of legislation:

None of these bills made it out of committee. |

|

EXPANDING HEALTH INSURANCE COVERAGE |

|

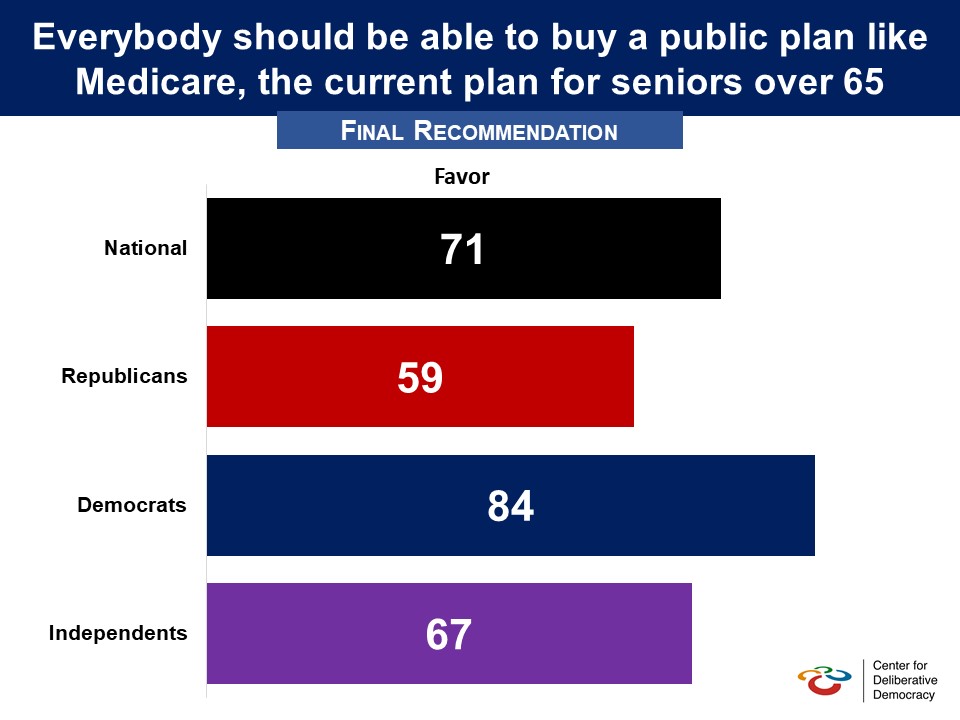

There has been increasing concern over the affordability of healthcare for people who are older and thus have more health risks and expenses, but are not yet eligible for Medicare. To address this concern, Members of Congress have introduced legislation that would lower the eligibility age for Medicare. In an in-person deliberation by Stanford University’s Center for Deliberative Democracy in September 2019, respondents were presented with the following proposal and arguments for and against it: Proposal: Everybody should be able to buy a public plan like Medicare, the current plan for seniors over 65. Argument in Favor: Medicare’s history shows that the government experiences much lower administrative costs than private insurance companies. This proposal would also allow new participants to obtain the high-quality care now available to Medicare beneficiaries. Allowing people of any age to buy in to Medicare would ensure that all Americans always have access to quality, affordable coverage regardless of employment status or the decisions of private insurance companies. This “Medicare buy-in” or “public option” would force insurance companies to compete with the government plan on price, potentially reducing costs across the board. Argument Against: With more enrollees and the same number of, or ever fewer, providers, medical care could be delayed or more difficult to access. Because Medicare pays lower rates to clinics, hospitals and doctors, this approach could compromise access to care. This could lead health care providers to demand higher payments from patients who retain private insurance, resulting in them paying significantly higher premiums for the same medical services. After receiving the briefing material, respondents deliberated on the proposal in-person. Finally, they were asked for their final recommendation. On a 0-10 scale, with 5 being “in the middle," 71% favored (6-10) the proposal, including 59% of Republicans and 84% of Democrats. Pre-Deliberation Poll

In an earlier poll in 2016 support was lower. Respondents were told that “One of the issues being debated in the election this year (2016) is whether or not the federal government should establish a government-sponsored health insurance program that would compete with private-health insurance plans. This is often called a public option and would be available only for those eligible for the Affordable Care Act.” A plurality of 48% favored “the government offering such a program with 42% opposed. Partisan breakouts were not provided. (September 2016, Politico/Harvard Public Health) Status of Legislation

None of these bills have made it out of committee. |

|

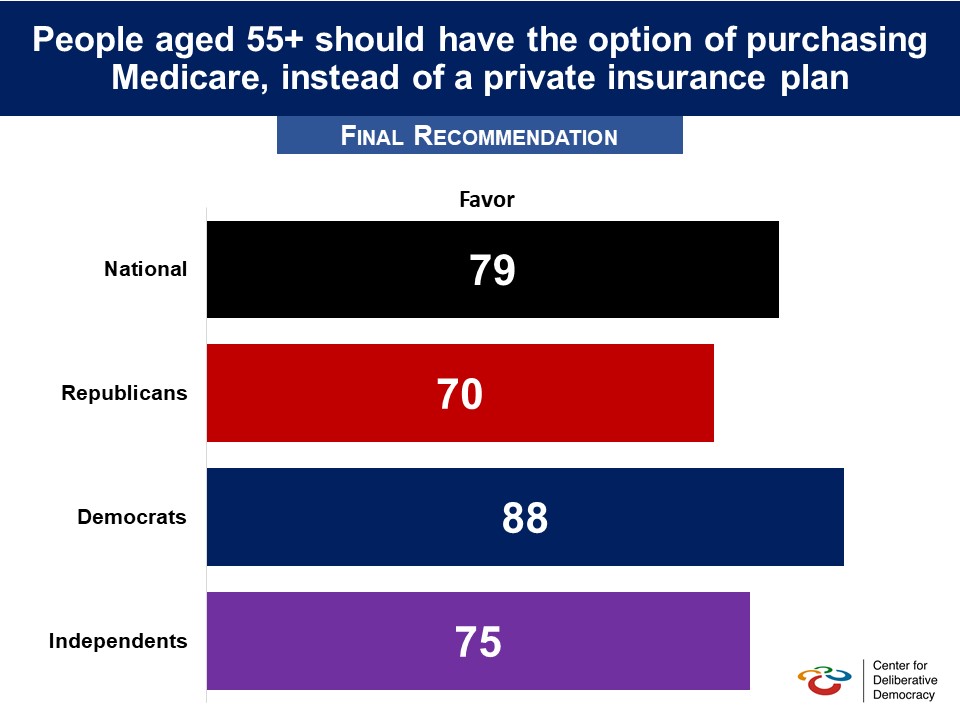

There has been increasing concern over the affordability of healthcare for people who are older and thus have more health risks and expenses, but are not yet eligible for Medicare. To address this concern, Members of Congress have introduced legislation that would lower the eligibility age for Medicare. In an in-person deliberation by Stanford University’s Center for Deliberative Democracy in September 2019, respondents were presented with the following proposal and arguments for and against it: Proposal: Americans aged fifty-five and older should have the option of purchasing Medicare, instead of a private insurance plan. Argument in Favor: Americans closer to retirement age typically have higher health care costs than younger individuals. This makes them more expensive to insure, resulting in higher premiums. Because these older adults have greater health care needs, they are more likely to enroll in health insurance than younger individuals. When older individuals make up a large share of the population enrolled in a plan, premiums increase for everyone. By allowing this group to buy into Medicare, the price of private plans could go down, because the remaining population enrolled in private insurance plans would be younger and healthier. Allowing individuals aged 55 and older to enroll in Medicare ensures they will always have access to quality, affordable health coverage. Americans 55-65 are likely healthier and less expensive for healthcare compared to those 65+. Allowing them to buy into Medicare will likely lead to a decrease in the average per capita healthcare spending in the patient pool, potentially lowering prices for patients in Medicare as well. Argument Against: By giving many people who are likely to be high consumers of health care — those 55 and older — access to Medicare, coverage and services to current recipients might be at risk. Just like a more general public option, a Medicare buy-in for people aged 55 and older is simply a way for the government to eventually put everyone into Medicare. And if the goal is to expand access to coverage, everyone regardless of age should be able to buy Medicare as an alternative to a private plan. After receiving the briefing material, respondents deliberated on the proposal in-person. Finally, they were asked for their final recommendation. On a 0-10 scale, with 5 being “in the middle”, 79% favored (6-10) the proposal, including 70% of Republicans and 88% of Democrats. Related Standard Polls

However when this possibility is set against adults 55 and over buying private insurance plans support is lower, though still a majority:

Status of Legislation |

|

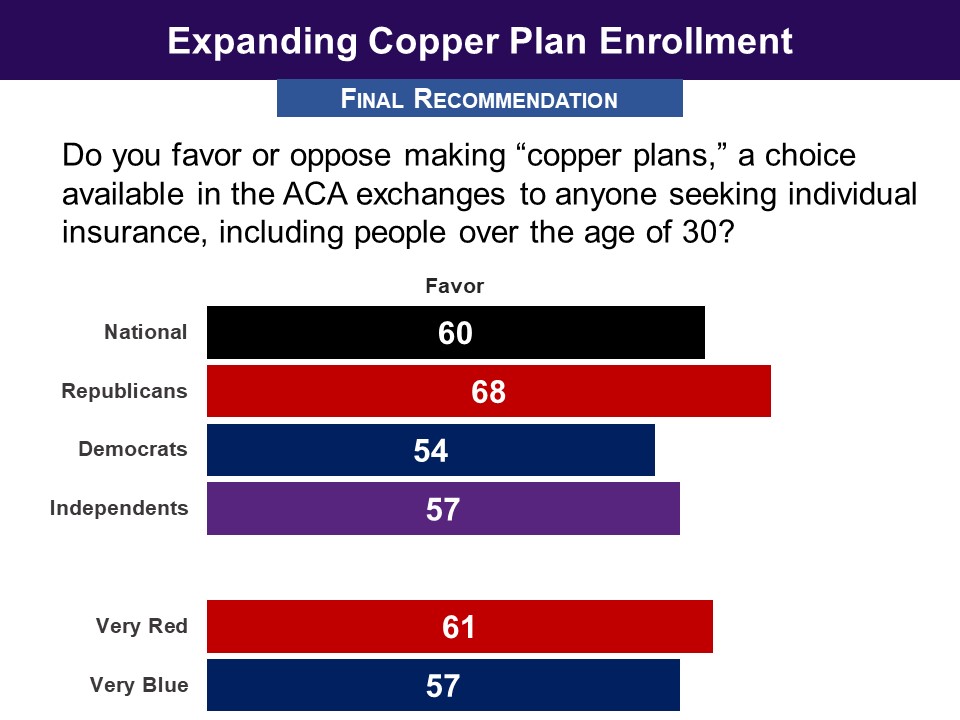

Survey: PPC, December 2017 Respondents were asked whether they favor, “making “copper plans,” a choice available in the ACA exchanges to anyone seeking individual insurance, including people over the age of 30.” A bipartisan majority of 60% were in favor, including 54% of Democrats, as well as 68% of Republicans.

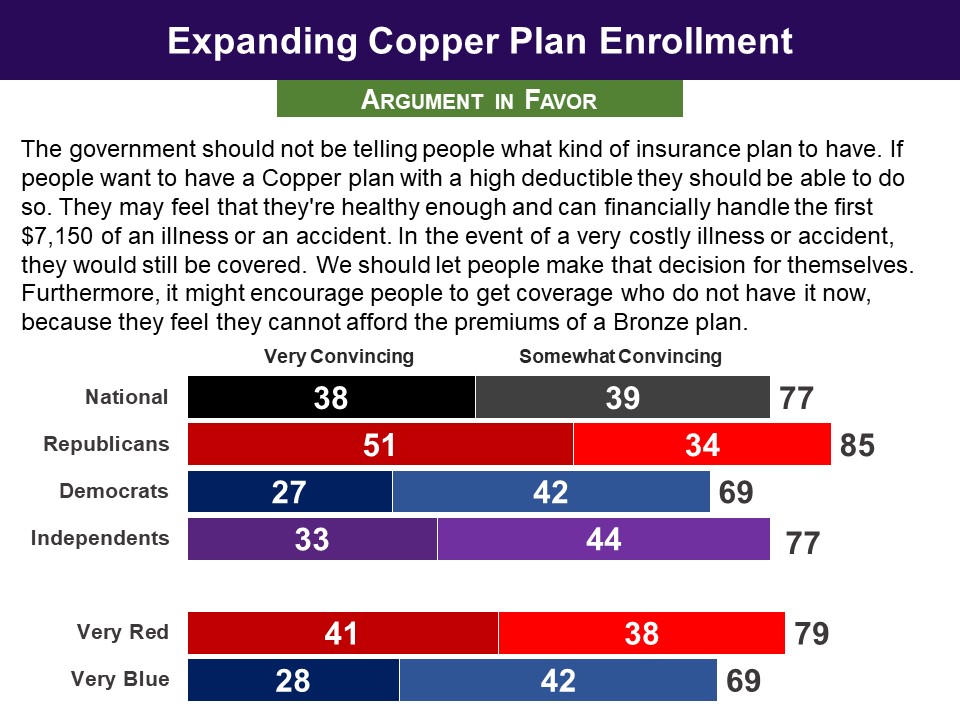

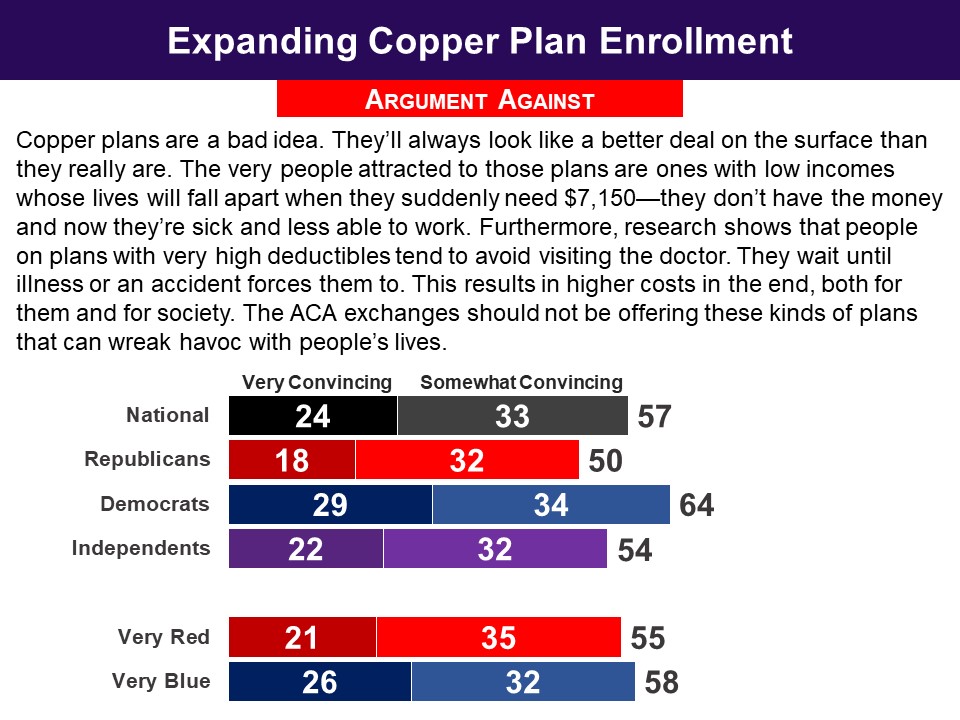

More Details Briefing One of the most controversial aspects of the ACA is that Americans age 30 and up cannot purchase what are called ‘copper plans,’ which have low premiums, but have a very high deductible--generally as high as $7,150. Members of Congress introduced the Bipartisan Health Care Stabilization Act of 2017, which would remove the ACA restriction on people age 30 and over purchasing low-cost ‘copper’ plans. Arguments The argument in favor was found convincing by 77%, including 69% of Democrats as well as 85% of Republicans. The argument against the proposal did not do as well--it was found convincing by 57%, including 50% of Republicans as well as 64% of Democrats.

Final Recommendation Asked for their final recommendation, 60% favored making copper plans available in the ACA exchanges to anyone seeking individual insurance, including people age 30 and older. This included 54% of Democrats, as well as 68% of Republicans.

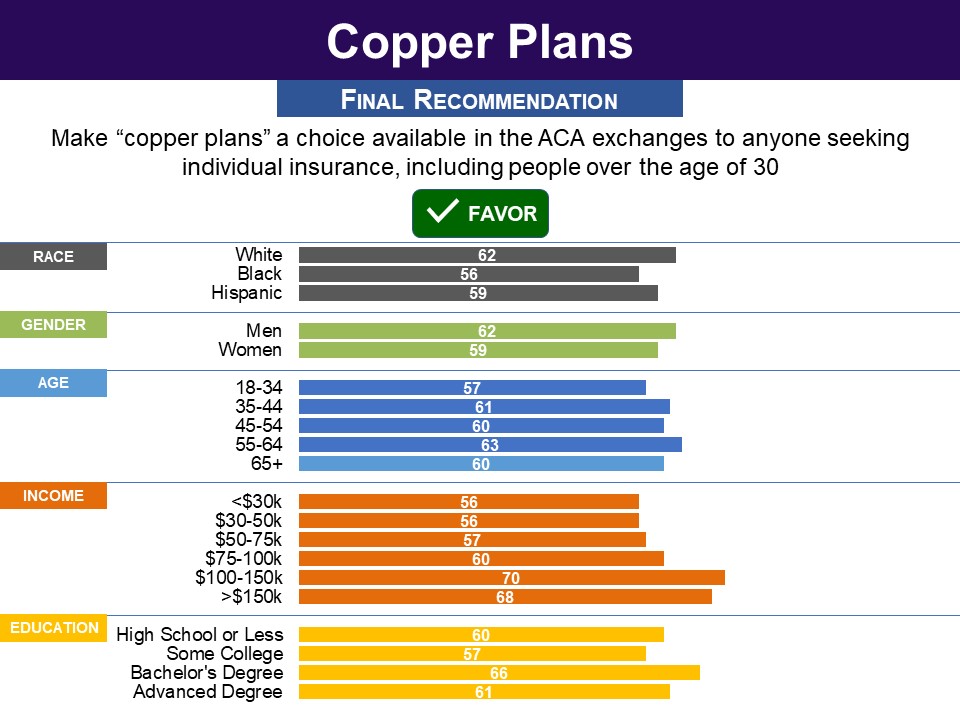

Demographics

Status of Legislation The proposal to repeal the Affordable Care Act rule prohibiting low-cost, high-deductible insurance plans, known as ‘copper plans’, from being purchased by people age 30 and over, was part of the Bipartisan Health Care Stabilization Act of 2018. The bill was never officially submitted as legislation. This proposal was also in the Fair Care Act (H.R. 1332), sponsored by Rep. Bruce Westerman in the 116th Congress. The bill did not make it out of committee. The proposal is not currently in any legislation. |

|

LOWERING ACA MARKETPLACE INSURANCE COST |

|

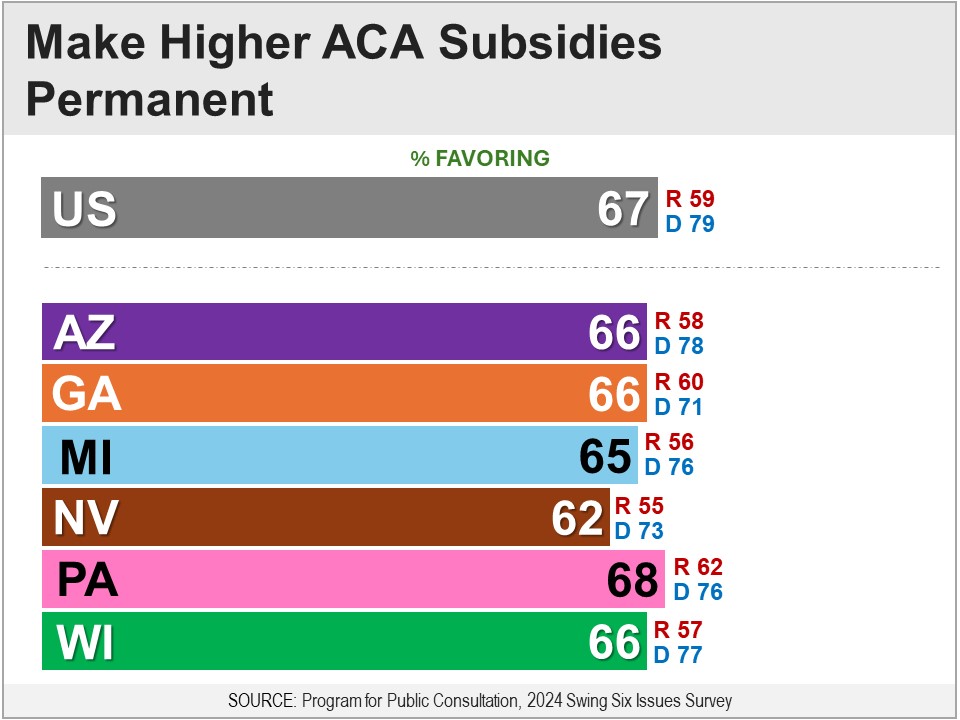

Survey: PPC, July 2024 Respondents were asked whether they favor the following proposal: Make permanent the law which has:

A bipartisan majority of 67% were in favor, including 59% of Republicans and 79% of Democrats.

More Details Briefing Respondents were presented a briefing on ACA subsidies that reduce the cost of premiums and deductibles: As you may know, the Federal government currently has a financial aid program that helps reduce the cost of health insurance for low and middle income households. Households can only get this financial aid if they cannot get insurance through their job, or from a government insurance plan like Medicaid (for households under the poverty line) or Medicare (for older adults). This program reduces household spending on healthcare, by:

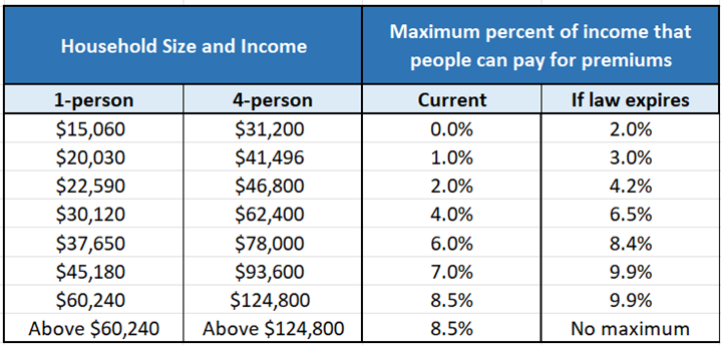

They were informed about the expansion of these subsidies in 2021 in response to the Covid pandemic: In 2021, in response to the Covid pandemic, Congress passed a law that increased this financial aid. to lower health insurance premiums and deductibles even more. It also expanded this financial aid to include more middle-income households, which resulted in about two million more people getting this aid. According to the Congressional Budget Office, this law has increased government spending by about $5 billion a year. However, this law is temporary and will expire in 2026, at which point the financial aid levels will go back down to what they were before 2021. They were told how that temporarily law changed premiums, which included a chart showing its effect on different income levels: Under the new law, very low-income households pay nothing for premiums, and middle-income households do not have to pay more than 8.5% of their income. Also, it expanded the number of people that can receive this aid, to include individuals who make over about $60,000 (families of four that make over about $125,000).

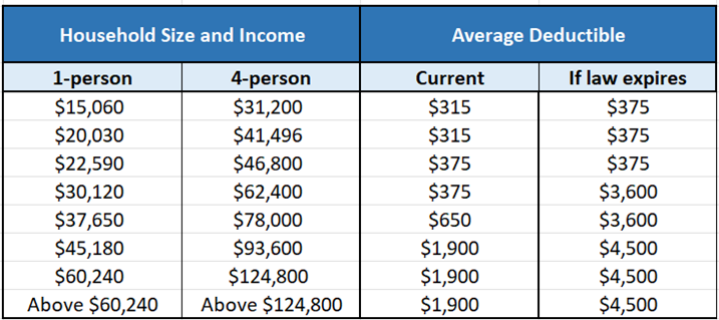

They were told how that temporarily law changed deductibles, which included a chart showing its effect on different income levels: Second, the law lowered the amount of the deductible. Unlike premiums, deductibles vary according to a number of factors.

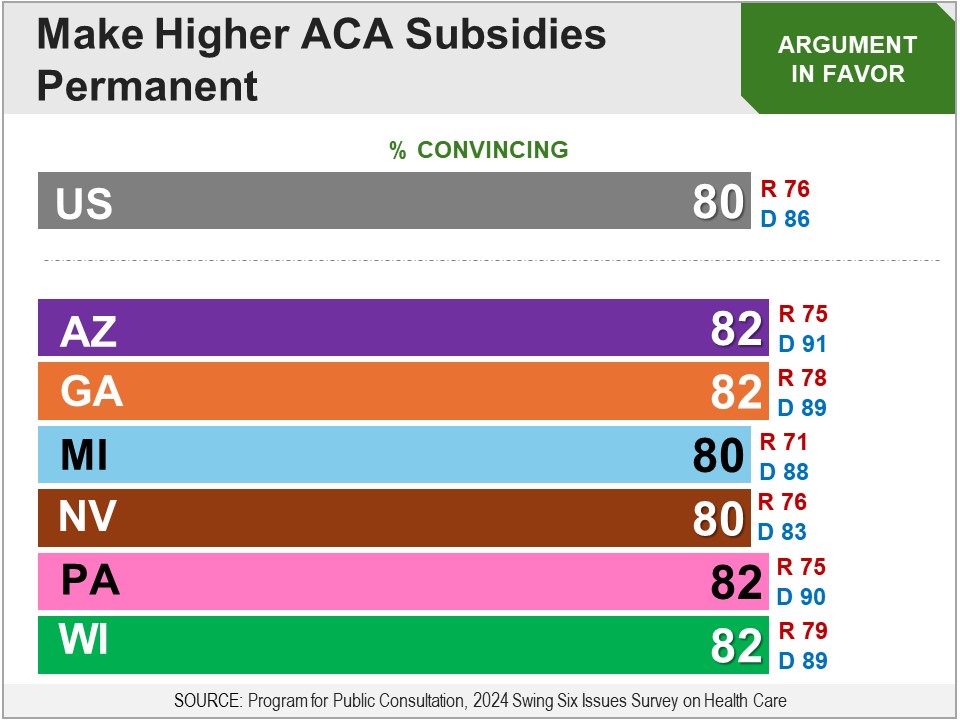

Arguments Respondents were then presented arguments for and against, “making permanent this increased financial aid for health insurance.” The argument in favor was found convincing by a very large bipartisan majority of eight-in-ten. The argument against did not do as well, but was still found convincing by a bipartisan majority of two-thirds.

Final Recommendation Finally, respondents were asked whether they favor the following: Make permanent the law which has:

A bipartisan majority of 67% were in favor, including 59% of Republicans and 79% of Democrats.

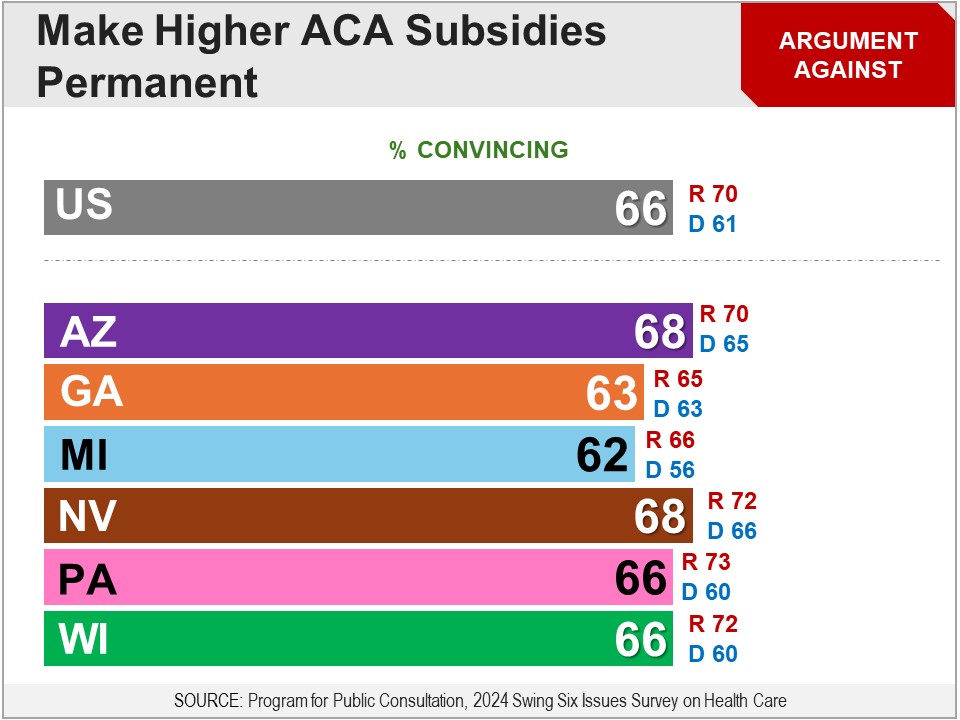

Results in Six Swing States The survey was also fielded in six swing states: AZ, GA, MI, NV, PA and WI. Across all swing states, bipartisan majorities of 62-68%, including 55-62% of Republicans and 71-78% of Democrats. Results from Deliberative Democracy Lab Subsidies for middle-income In an in-person deliberation by Stanford University’s Center for Deliberative Democracy in September 2019, respondents were presented with the following proposal: The federal subsidies in the ACA that help the middle class should be expanded to include more people. After receiving the briefing material and evaluating arguments for and against, respondents deliberated on the proposal in-person. Finally, they were asked for their final recommendation. On a 0-10 scale, with 5 being “in the middle”, 72% favored (6-10) the proposal, including 51% of Republicans and 87% of Democrats. Subsidies for low-income Respondents in that same deliberative poll were presented another proposal: The federal subsidies in the Affordable Care Act that help the poor should be increased A majority of 60% favored the proposal, including 82% of Democrats. Among Republicans, just 33% were in support, but 60% did not oppose the proposal (5-10). Related Standard Polls Bipartisan majority has supported extending the ACA subsidies:

However, when told that the proposal is part of Kamala Harris’ plan, support dropped substantially among Republicans:

Given the options to increase, decrease or not change spending on healthcare subsidies for people who can not afford health insurance, a majority of Democrats have preferred increasing spending, but less than half of Republicans:

Status of Legislation The proposal to expand healthcare subsidies to cover more middle-income people was passed in the covid-relief American Rescue Plan sponsored by Rep. John Yarmouth in the 117th Congress. It passed the House with 220D voting in favor, and 210R and 1D voting against; and passed the Senate with 48D and 2I voting in favor and 49R voting against. Those subsidy increases were temporary, and in 2022 were extended for another three years by the Inflation Reduction Act, sponsored by Rep. John Yarmouth. It passed the House with 220D voting in favor, and 212R and 1D voting against; and passed the Senate with 48D, 2I and the Vice President voting in favor, and 50R voting against. In the 118th Congress, a proposal to make permanent the new ACA subsidies was put forward in the Health Care Affordability Act by Rep. Lauren Underwood (H.R. 9774) and Sen. Jeanne Shaheen (S. 5194). The bill did not make it out of committee. |

|

PRESERVING ACA RULES |

|

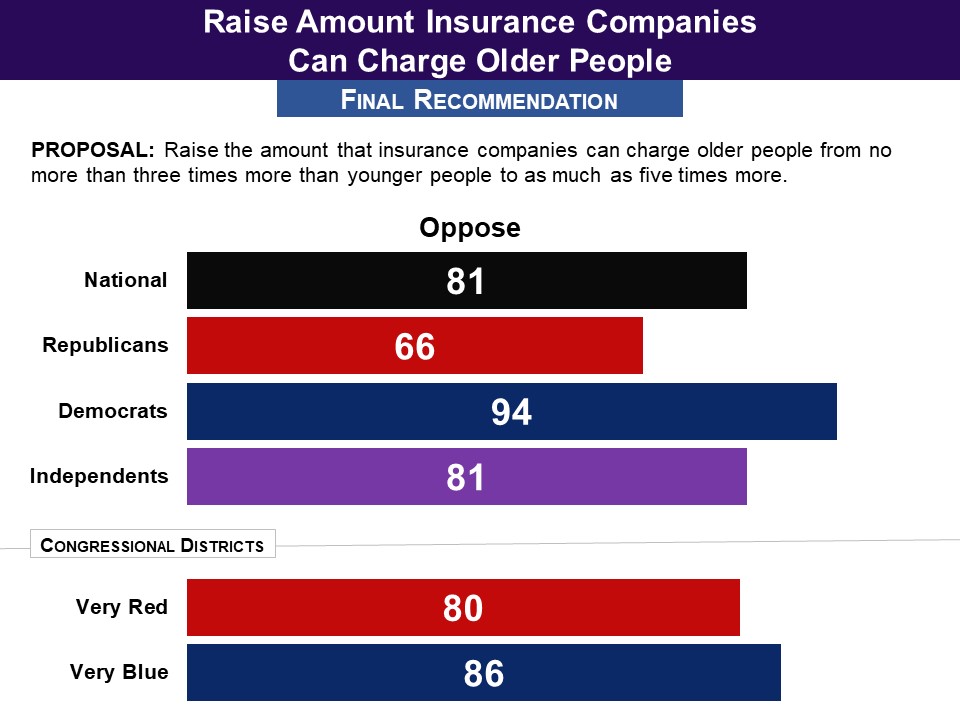

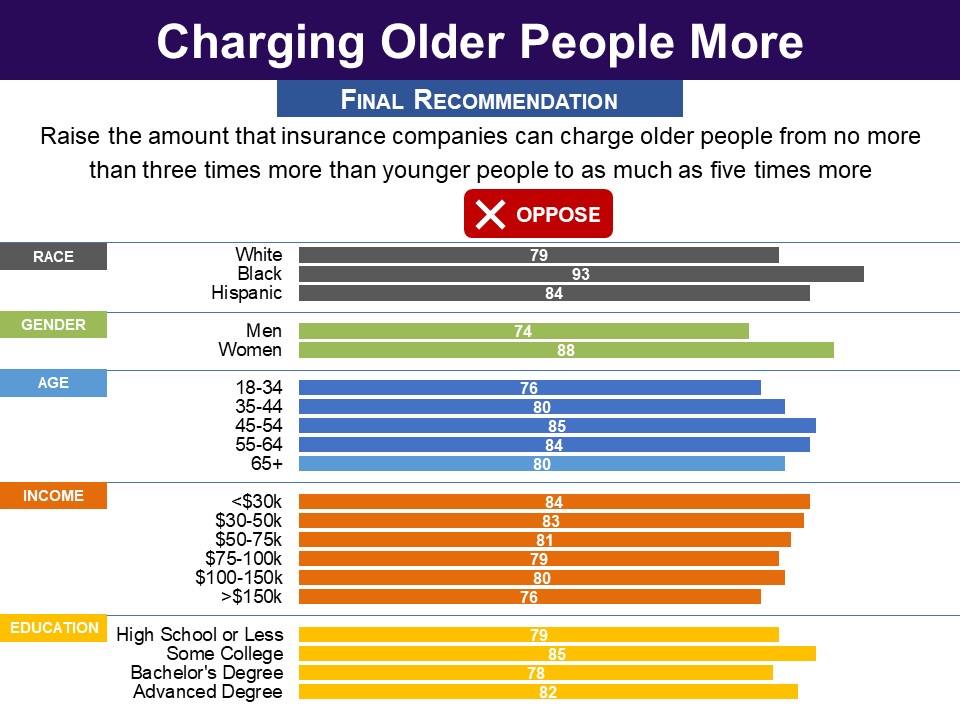

Survey: PPC, June 2017 Respondents were asked whether they favor the following proposal, which would undo a provision of the Affordable Care Act: Raises the amount that insurance companies can charge older people from no more than three times more than younger people to as much as five times more. A bipartisan majority of 81% were opposed, including 66% of Republicans and 94% of Democrats.

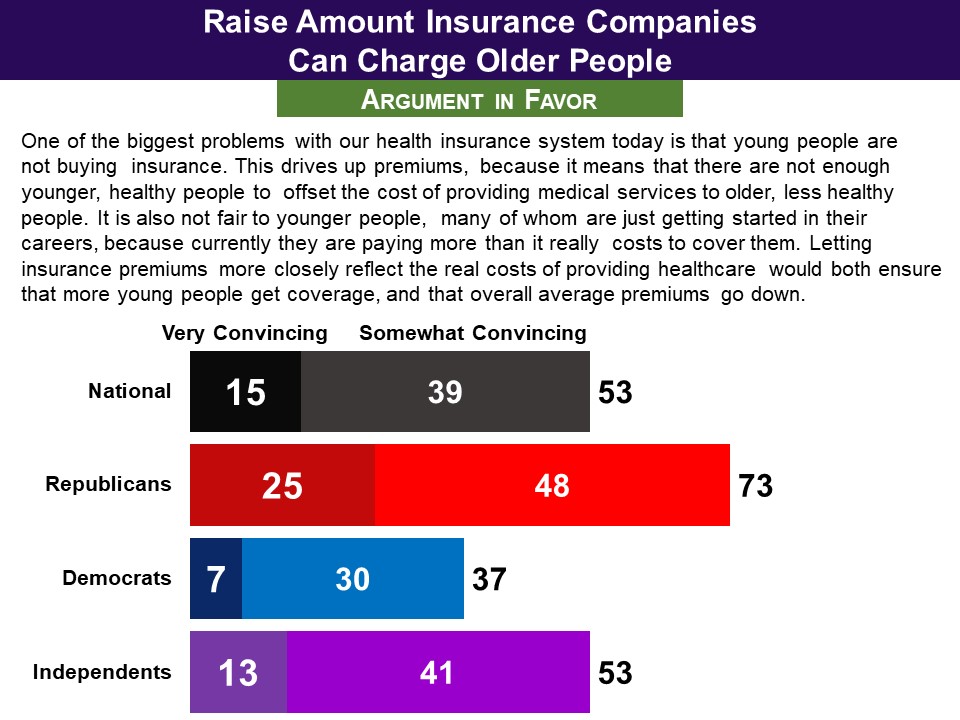

More Details Briefing Respondents were first told the rationale for insurance companies charging older people more—which is a feature of both current law and proposed law: As you may know, older people tend to use more health services than young people. Therefore,insurance companies charge older people higher insurance rates‐‐specifically people aged 50‐64 who are not yet on Medicare. Before current law went into effect, insurance companies generally charged about five times more for older people than for younger people. Respondents learned that currently, insurance companies are not allowed to charge older people more than three times more than younger people, while the proposed law would raise this limit to five times more. They were told that CBO has estimated the most likely effects of this increase would be to:

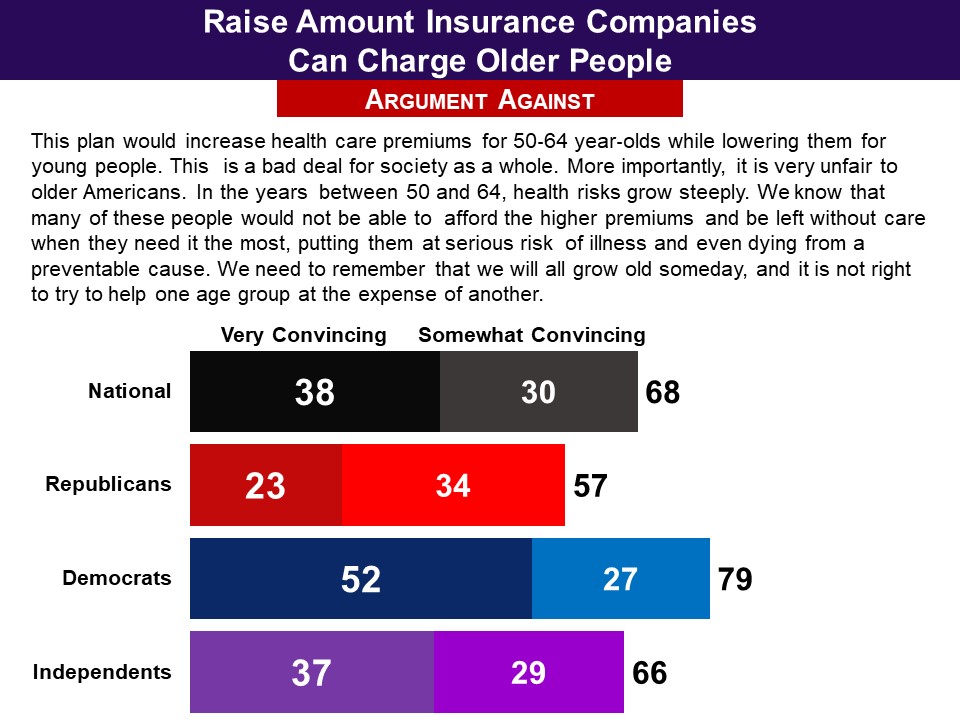

Arguments The argument in favor of this provision was convincing to a modest majority of 53%. There was a sharp partisan difference with 73% of Republicans finding it convincing, but only one third of Democrats. The argument for preserving current law was found convincing, by 68%, including 57% of Republicans and four in five Democrats. Interestingly, the argument was found convincing by a smaller majority than the one that ultimately opposed the provision, suggesting the argument may not have fully captured some key reasons respondents opposed the provision.

Final Recommendation Finally, a very large bipartisan majority opposed the proposal to allow insurance companies to charge older people as much as five times more than younger people. Four in five overall (81%) opposed it, including a robust 66% of Republicans as well as 94% of Democrats and 81% of independents.

Demographics

Related Standard Polls Large bipartisan majorities have opposed allowing insurance companies to charge older insurees more than is currently allowed under the Affordable Care Act rule, with the question not specifying the the current or proposed differentials:

Status of Legislation The proposal to increase the amount that health insurance companies can charge older insurees relative to younger ones, from three times to five times, was part of the American Health Care Act of 2017 (H.R. 1628), sponsored by Rep. Diane Black (R) in the 115th Congress. This bill passed the House, and then failed in the Senate. In the House, 217 Republicans voted in favor, and 20 Republicans and 193 Democrats voted against. In the Senate, 49 Republicans voted in favor, and 2 Republicans and 49 Democrats voted against. A bill to fully repeal the Affordable Care Act, which would remove protections for people with pre-existing conditions, was in the Responsible Path to Full Obamacare Repeal Act by Rep. Andy Biggs (H.R. 112) in the 118th Congress. It did not make it out of committee. |

|

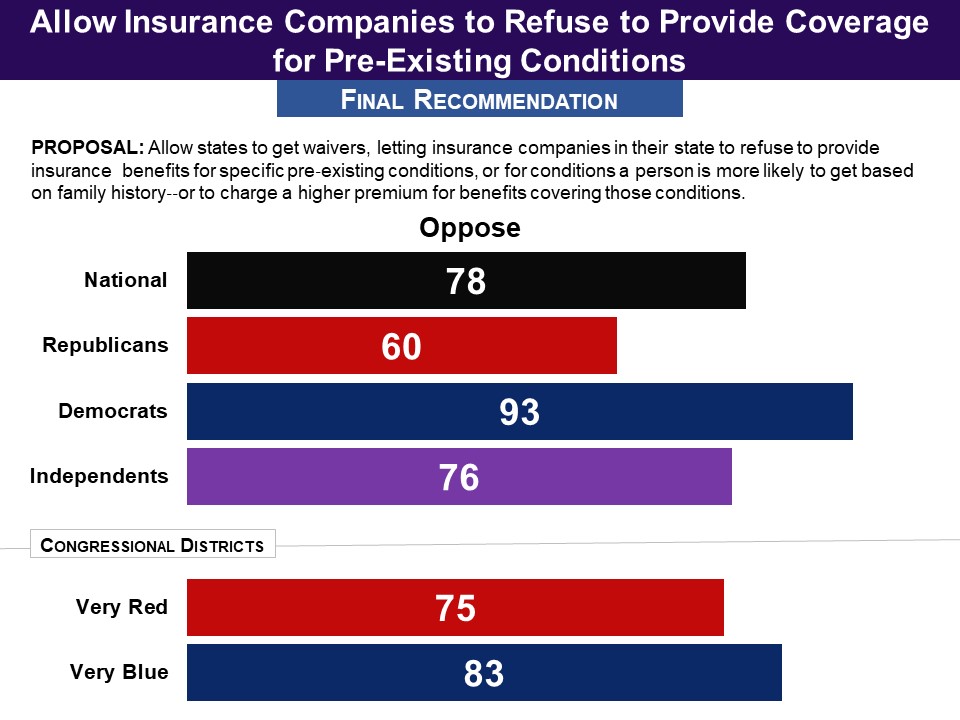

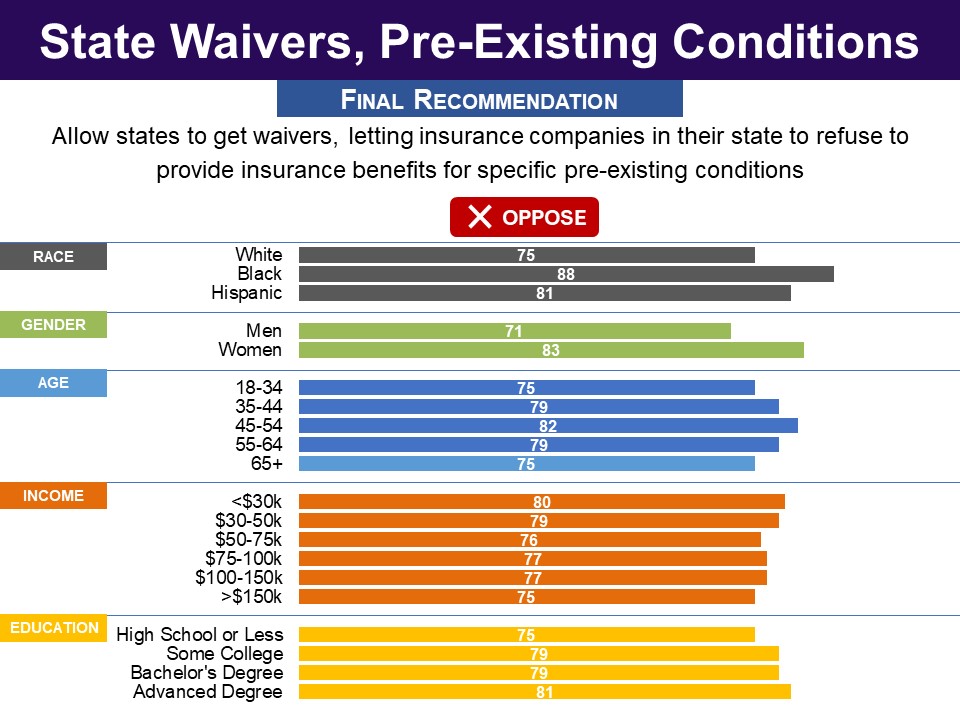

Survey: PPC, June 2017 Respondents were asked whether they favor the following proposal, which would undo a provision of the Affordable Care Act: Allows states to get waivers, letting insurance companies in their state to refuse to provide insurance benefits for specific pre‐existing conditions, or for conditions a person is more likely to get based on family history‐‐or to charge a higher premium for benefits covering those conditions. A bipartisan majority of 78% were opposed, including 60% of Republicans and 93% of Democrats.

More Details Briefing Respondents were first reminded that under current law, insurance companies cannot decline to cover someone with a pre‐existing health condition or to charge them a higher premium. They were told: The proposed law gives states the option to get a waiver that would let insurance companies refuse to provide insurance benefits for specific pre‐existing conditions, or for conditions a person is more likely to get based on family history‐‐or to charge a higher premium for benefits covering those conditions. They then learned about the CBO’s estimate of the outcome should this provision take effect:

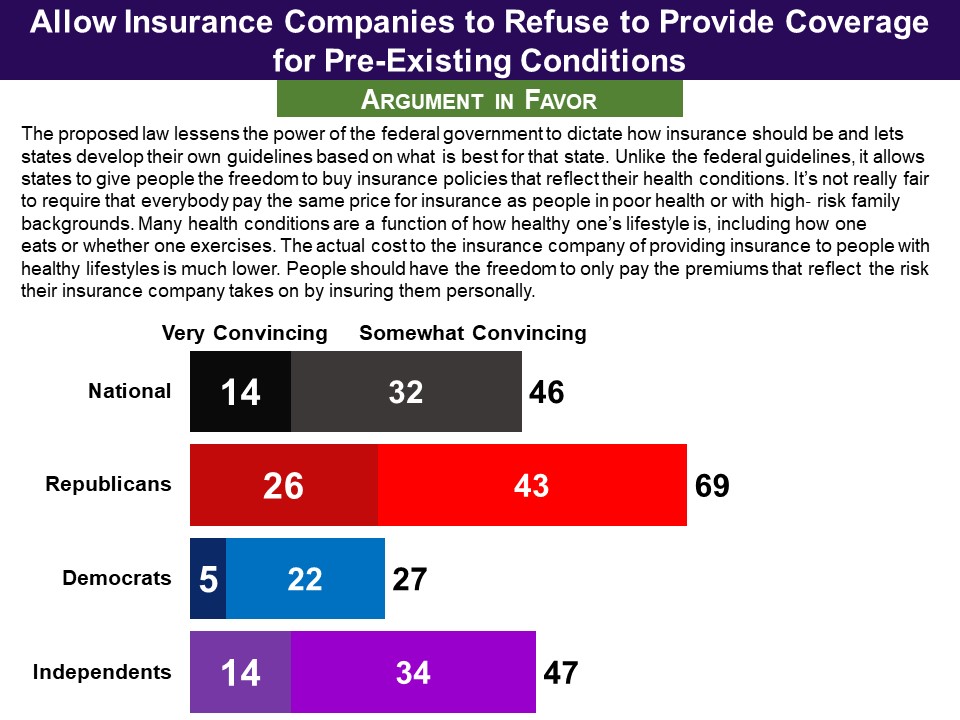

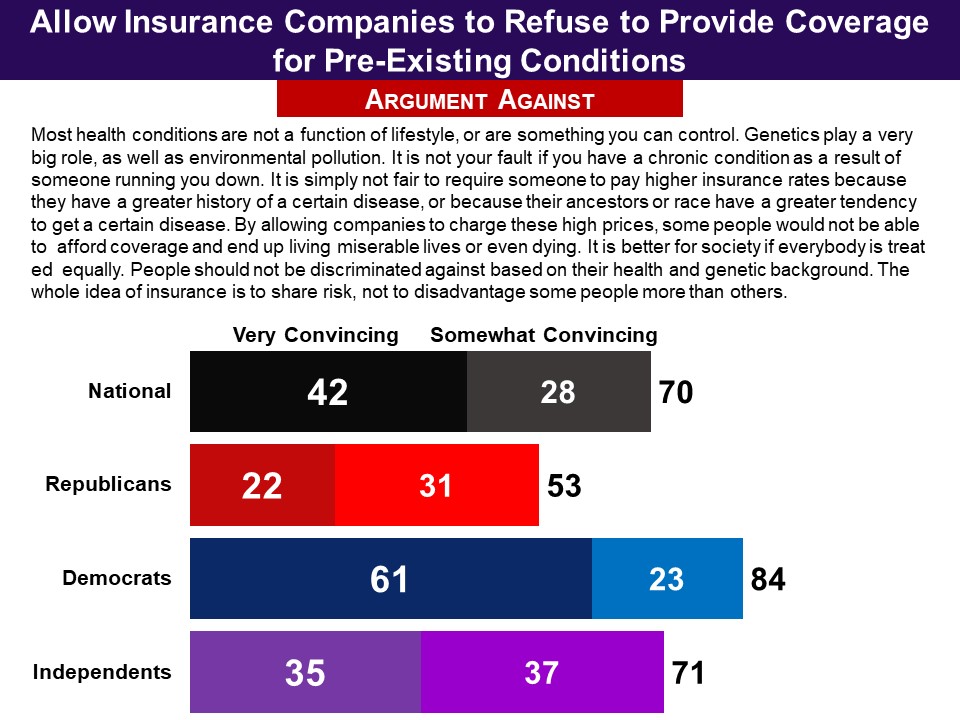

They also learned that in compensation, the proposed law would dedicate funds to help states set up high‐risk pools for such people—but that CBO estimated the amount set aside would be insufficient and some people would wind up without coverage. However, premiums would be lower for the majority of people with lower health risks, and some of these would get insurance who would not have done so otherwise. Arguments The argument supporting the proposal was found convincing by 46%, including just a quarter of Democrats and just under half of independents. However, seven in ten Republicans found it convincing. The argument for preserving current law was found convincing by 70%, including 53% of Republicans, 84% of Democrats and seven in ten independents.

Final Recommendation In conclusion, a large bipartisan majority rejected the proposal to allow state waivers from the ACA, allowing health insurance companies to consider pre‐existing conditions. This was opposed by 78% nationally, including 60% of Republicans and 93% of Democrats. Interestingly, for Republicans, though the argument in favor did better than the argument against, 60% opposed the proposal‐‐as did 76% among independents and 93% among Democrats.

Demographics

Related Standard Polls Large bipartisan majorities have consistently approved of the ACA’s provision prohibiting insurance companies from considering pre-existing conditions when determining premiums and coverage:

Status of Legislation The proposal to give states waivers for allowing health insurance companies to consider pre-existing conditions when determining premiums and coverage was part of the American Health Care Act of 2017 (H.R. 1628), sponsored by Rep. Diane Black in the 115th Congress. This bill passed the House, and then failed in the Senate. In the House, 217 Republicans voted in favor, and 20 Republicans and 193 Democrats voted against. In the Senate, 49 Republicans voted in favor, and 2 Republicans and 49 Democrats voted against. |

|

MEDICAID |

|

Survey: PPC, April 2025 Asked whether federal spending on Medicaid should be reduced, kept the same, or increased, a bipartisan majority of 81% favored increasing or keeping it the same (Republicans 75%, Democrats 86%). A modest majority (55%) favored increasing spending on Medicaid, which respondents were informed would allow Medicaid to enroll more people or cover more services. A majority of Democrats (65%) want to increase spending, as do nearly half of Republicans (49%).

More Details Briefing Respondents were informed that Medicaid is the government health insurance program that covers low-income households: those earning at most 138% of the Federal poverty line in most states (with a slightly higher income cutoff for children, people over 65 and people with disabilities). Medicaid covers about 71 million people, or around one-fifth of the US population, including about four in ten children. They were also informed that the Federal government covers about two-thirds of the cost of Medicaid – $608 billion last year or about ten percent of the federal budget – and state governments cover the other third. Arguments Respondents evaluated one pair of arguments for and against reducing spending on Medicaid, and another pair for and against increasing spending, which they were informed would allow Medicaid to cover more people and/or more services. The arguments against reducing spending and in favor of increasing spending did very well (81 and 82%), including among both Republicans and Democrats. The arguments in favor of reducing spending and against increasing spending did much worse (55 and 56%), with less than half of Democrats finding them convincing but a majority of Republicans.

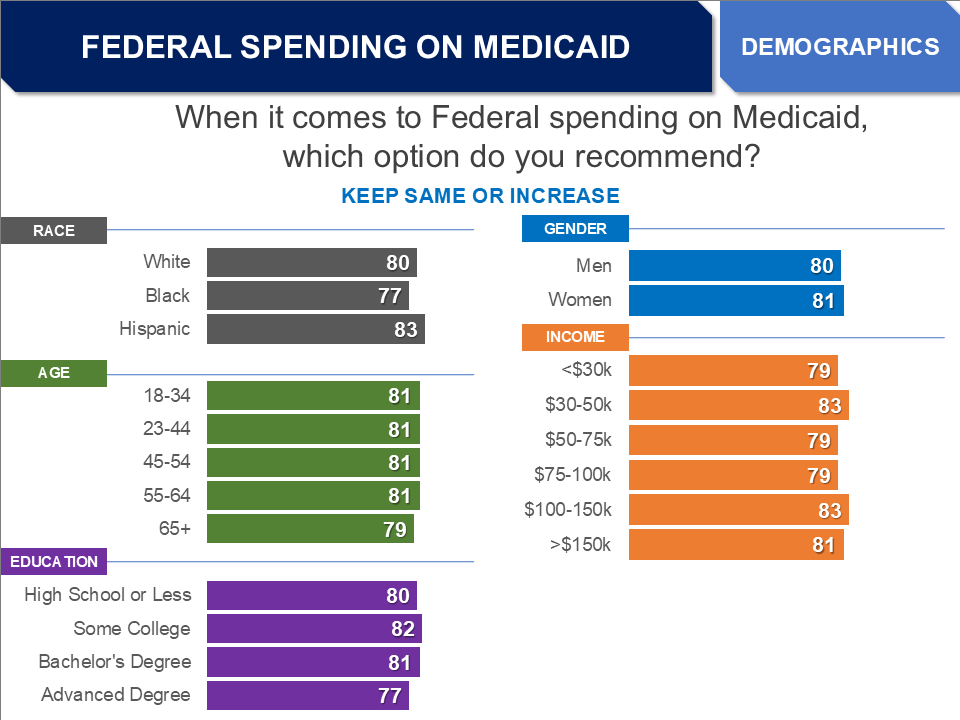

Final Recommendation In the end, respondents were asked, “when it comes to Federal spending on Medicaid, which option do you recommend,” and given a 7-point scale from “reduce a lot” to “increase a lot”, with “keep the same” in the middle. A bipartisan majority of 81% favored federal spending on Medicaid being increased or kept the same, including 75% of Republicans and 86% of Democrats. A modest majority (55%) favored increasing spending on Medicaid, which respondents were informed would allow Medicaid to enroll more people or cover more services. This included a majority of Democrats (65%) and nearly half of Republicans (49%).

Demographics

Standard Polling Standard polling has consistently, over the last several decades, found very large majority support for spending on Medicaid to be increased or kept the same:

When respondents are presented a proposal to cut Medicaid spending, without being given an option to increase or keep it the same, a smaller but still very large and bipartisan majority disagree with cutting Medicaid:

When a proposal to cut Medicaid spending is presented as part of the One Big Beautiful Bill, which was supported only by Republicans in Congress and President Trump, a majority are still opposed, but a smaller majority likely due to more Republicans being in favor (partisan breakouts were not provided unfortunately):

|

|

Survey: PPC, April 2025 Having their state be part of the Medicaid expansion program is favored by a large bipartisan majority of 83%, including 79% of Republicans and 91% of Democrats. In the ten states that have not expanded Medicaid, 75% favor their state government opting in to the program and paying the required ten percent of extra costs (Republicans 69%, Democrats 82%). In the states that have already expanded Medicaid, 87% favor their state government continuing to be part of the program (Republicans 83%, Democrats 94%).

Demographics

Briefing Respondents were informed how the Medicaid expansion program works: As you may know, the Federal government has a program to help states pay for expanding Medicaid to more people – those earning a little above the Federal poverty line – but only if states agree. Here is how this works: For states that choose to expand Medicaid, the Federal government pays 90% of the cost, and the state government pays for the other 10%. So far, 40 states have agreed to this expansion. Depending on their size, states pay an additional few hundred thousand to a few million extra dollars a year. As a result, 20 million more people have been getting Medicaid coverage in those states, or about 8% of their populations on average. Ten states have declined the option to expand Medicaid. Past PPC Findings A 2017 PPC Survey on the Affordable Care Act found only a slightly lower level of support for the Medicaid expansion program in general. At the time, the federal government would cover the entire cost of a state expanding Medicaid. Currently, the federal government covers 90 percent. Asked how acceptable they find the program, a bipartisan majority of 74% said acceptable or tolerable, including 76% of Republicans and 72% of Democrats. Related Standard Polling Standard polling has found bipartisan majority support for expanding Medicaid in their state, including among residents in states that have not expanded Medicaid:

|

|

SUBSTANCE ABUSE AND MENTAL HEALTH |

|

Survey: PPC, June 2022 Before evaluating any proposals, respondents were presented an overview of substance use disorder: how it is defined, its prevalence, its effects on users’ health, and its cost to society. First, they were presented a definition of substance use disorder, based on the DSM-V, as follows: A person has a substance use disorder if they meet some of the following criteria:

They were told that, “there are millions of Americans who have a substance use disorder,” and that, “since the covid pandemic began, it is estimated that the number of people misusing alcohol and drugs has increased. How addiction works was then explained: There are various ways that people start using substances before developing a substance use disorder or an addiction to the substance. They may start by drinking alcohol in an ordinary fashion, occasionally taking drugs for recreational purposes, or taking prescribed pain killers. Some people may use substances to deal with underlying problems such as depression or anxiety for which they are not getting treatment. This is sometimes called self-medication. Most people do not become addicted when they use such substances. Some people are born with a genetic tendency to become addicted. Traumatic experiences, such as childhood abuse or military combat, can also increase the tendency to addiction. For people who become addicted, the substance has an impact on their brain functioning, making it harder for them to resist using the substance and difficult to stop without treatment. In recent years, as opioids were prescribed more liberally, there was a significant increase in the number who became addicted and started using unprescribed drugs once their prescriptions ran out. As a result, opioids are now prescribed in a more limited way. However, there are still large numbers of people still dealing with their resulting opioid addiction The health consequences of substance use disorders were then summarized: Another side effect of substance misuse and addiction is its negative effect on people’s health, including serious effects on people’s heart, lungs, liver and other vital organs. These effects can even be fatal over time. People can also catch lifelong diseases, such as HIV and Hepatitis, when they share needles or other tools used to take drugs. People can also overdose from drugs or alcohol, which can result in death. Over the last couple decades, there has been a large increase in the number of deaths from drug overdoses. In the year 2020, around 100,000 people died from drug overdoses, more than triple what it was in 2000. Three quarters of those overdose deaths are from the use of opioids. In addition, each year about 90,000 people die from alcohol misuse. The last part of the briefing explained the societal costs of substance use disorder: Substance use disorders also cost society as a whole – over $400 billion a year according to the National Institute of Health. This includes :

In addition to these costs, the deaths from overdoses have substantial economic consequences. |

|

|

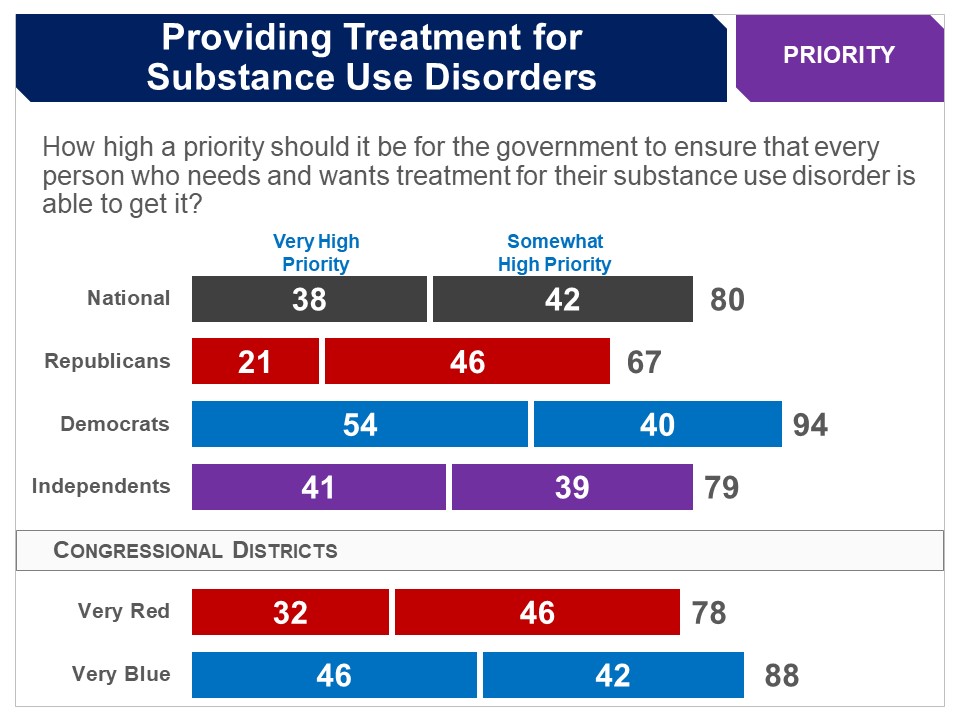

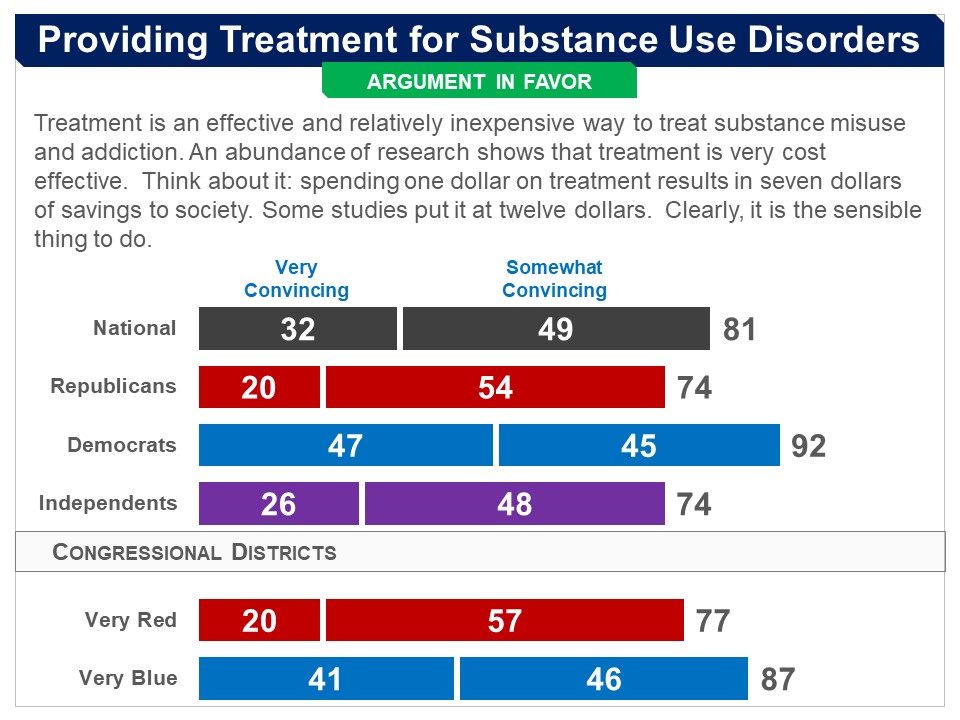

Survey: PPC, June 2022 Respondents were asked, “how high a priority should it be for the government to ensure that every person who needs and wants treatment for their substance use disorder is able to get it.” Eighty percent said a high priority (very high 38%), including 67% of Republicans (very high 21%) and 94% of Democrats, with a majority of Democrats saying very high (54%). More Details Briefing After being presented a briefing on substance use disorder (see "Design of Survey" above), respondents were introduced to substance use disorder treatment, as follows: Treatment may involve counseling, medication, and possibly staying in a rehabilitation (or ‘rehab’) center for intensive treatment. Research finds that the majority of people who go through a treatment program reduce or stop abusing drugs and alcohol and improve their ability to function in their social lives and remain employed. Treatment, however, is often an ongoing process. About half of the people who enter treatment start misusing substances again and need to return to treatment or receive additional treatment. They were told of current government efforts to increase treatment, and its cost-effectiveness: To help increase the amount of treatment available, the federal government provides cities and states with money to develop and operate treatment programs, and to train healthcare workers in substance use disorder treatment. Spending money on treatment has proven to be cost-effective. The National Institute of Health estimates that for every dollar spent on treatment, there are $7 in savings related to healthcare, criminal justice, and economic productivity. They were then informed of the ongoing “treatment gap”: Despite the spending on treatment, there are still many people who need and want treatment but cannot get it. There are about 1 million people who need and want treatment, or more treatment, but are not getting it. Before turning to specific proposals for increasing treatment, respondents evaluated general arguments for and against “whether government spending on treatment should be increased so that all people who need and want treatment can get it.” Arguments The arguments in favor were found convincing by very large majorities, overall and among both Democrats and Republicans. The arguments against were found convincing by less than half; and only one con argument was found convincing by a majority of Republicans. Final Recommendation Asked, “how high a priority should it be for the government to ensure that every person who needs and wants treatment for their substance use disorder is able to get it,” 80% said a high priority (very high 38%), including 67% of Republicans (very high 21%) and 94% of Democrats, with a majority of Democrats saying very high (54%). |

|

Survey: PPC, July 2024 After evaluating the arguments for and against increasing funding for substance use disorder treatment (see above), respondents were presented a proposal that would increase federal spending on treatment by investing an additional:

They were told that, “experts estimate that increasing spending by this amount would likely enable nearly all people who need and want treatment for their substance use disorder to get it.” In the end, 80% favored this proposal, including 77% of Republicans, 86% of Democrats and 71% of independents.

|

|

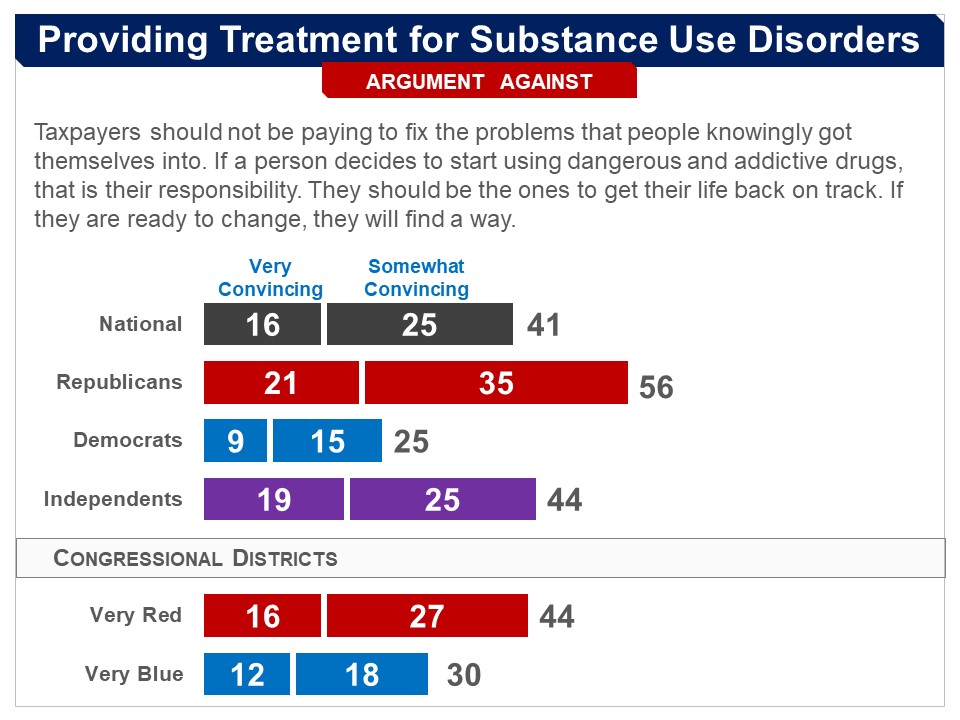

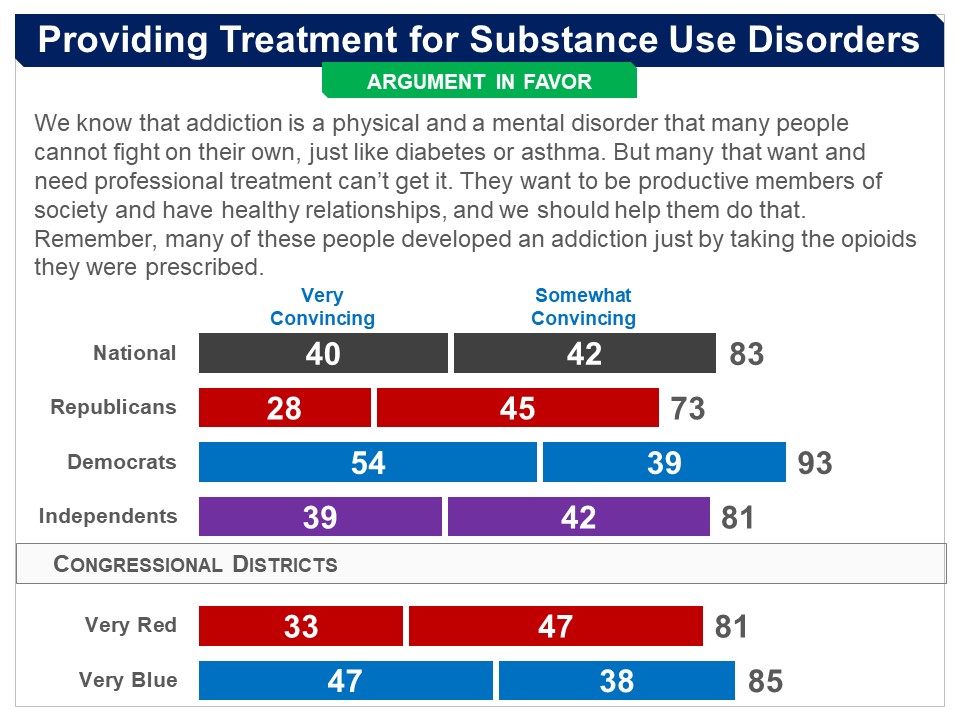

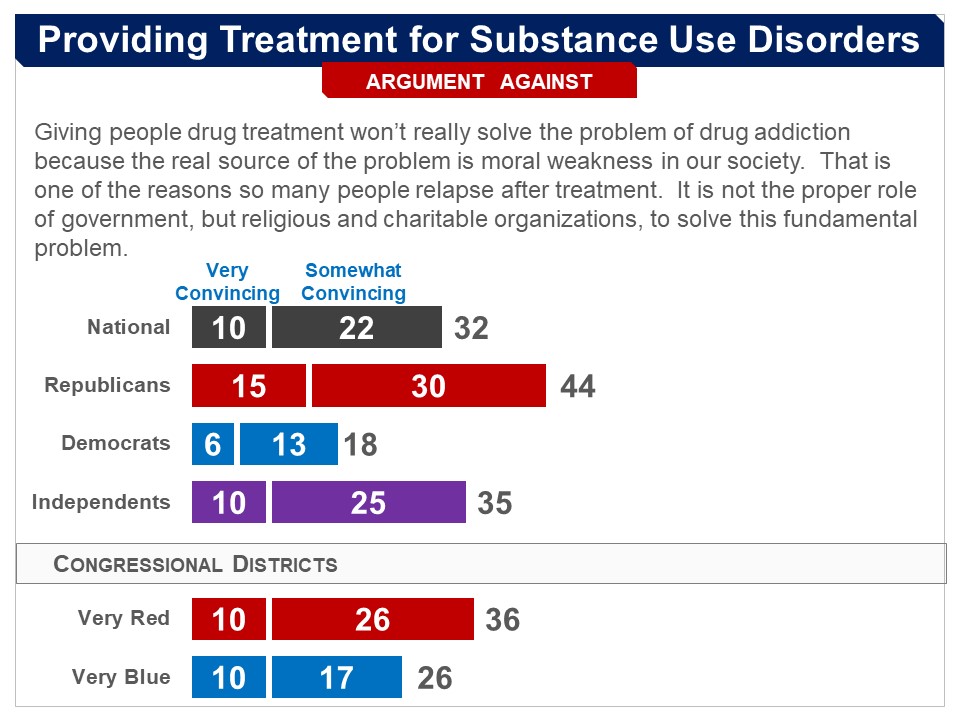

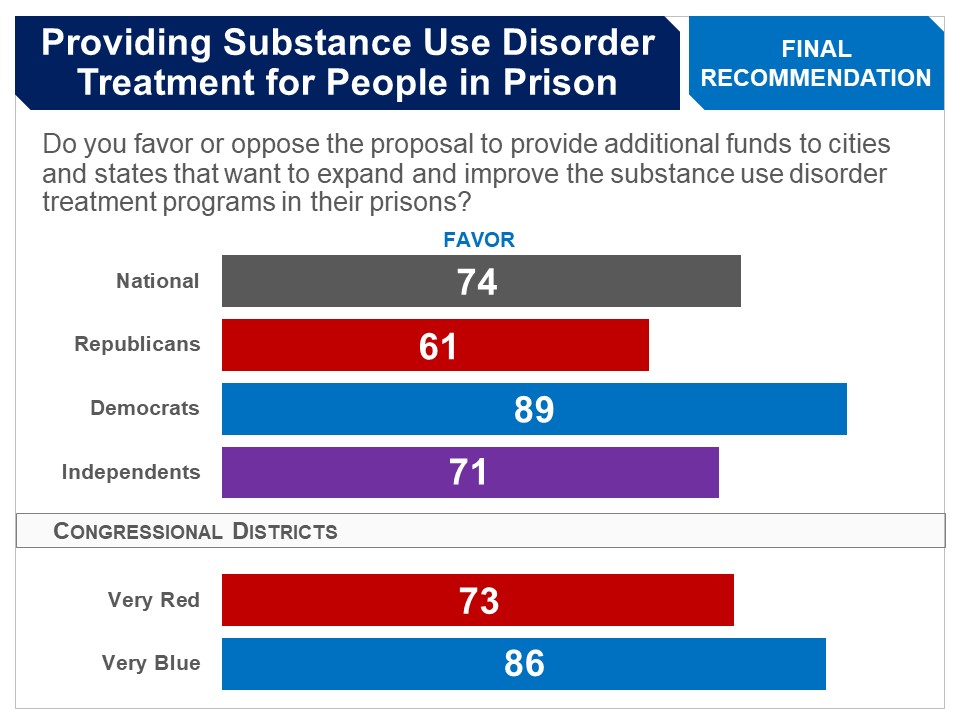

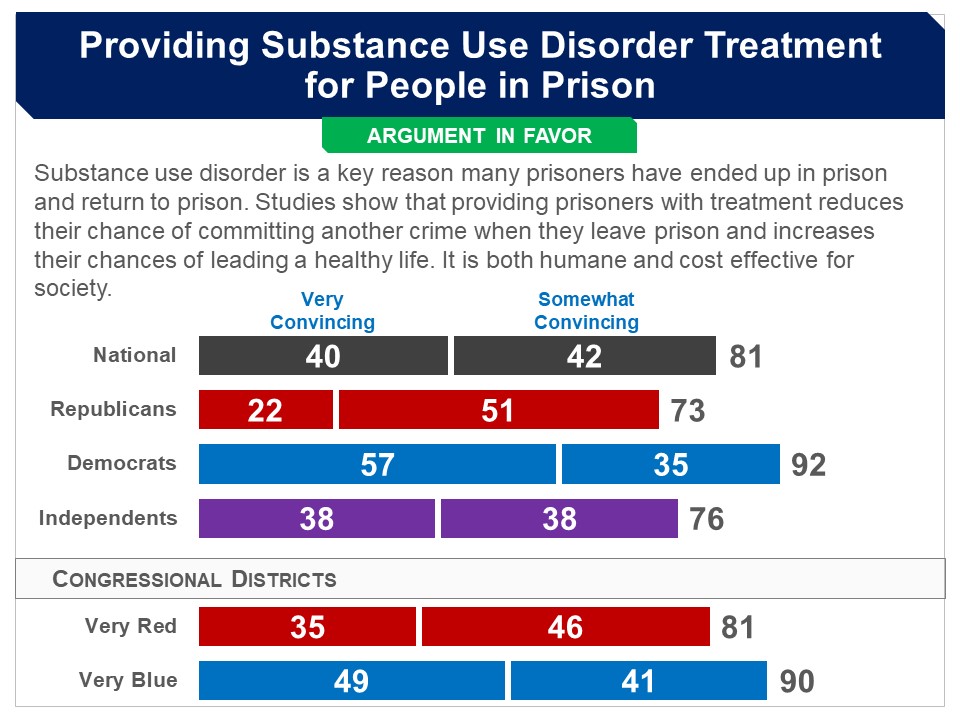

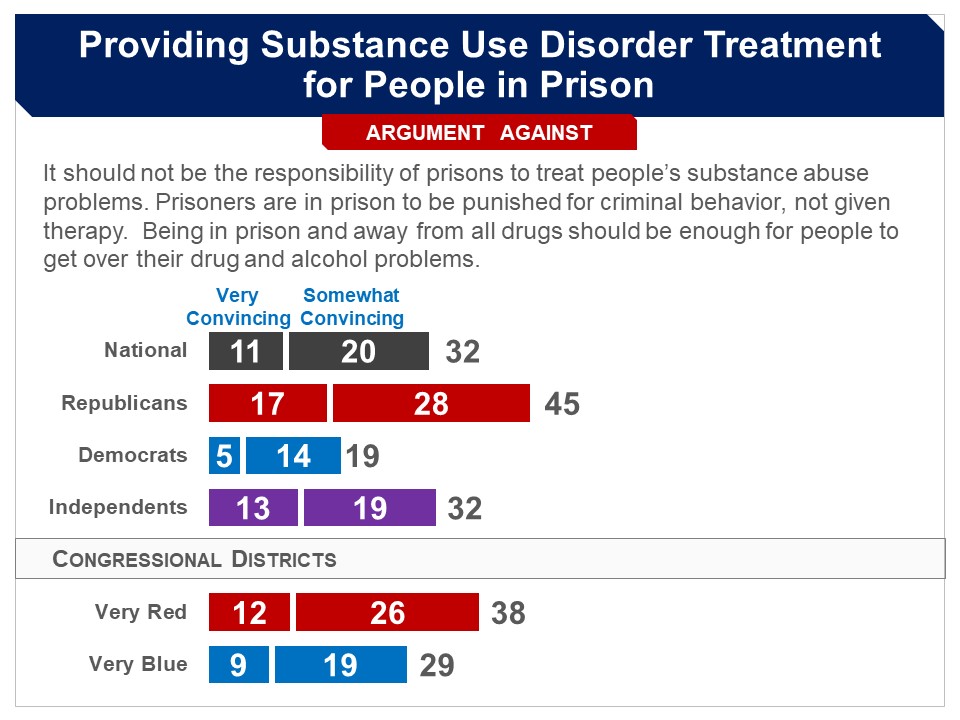

Survey: PPC, June 2022 Respondents were asked whether they favor the following: Provide additional funds to cities and states that want to expand and improve the substance use disorder treatment programs in their prisons. A bipartisan majority of 74% favored the proposal, including 61% of Republicans, 89% of Democrats and 71% of independents. More Details Briefing Respondents were presented a briefing on the prevalence of substance use disorders and treatment programs in prisons: According to the latest estimates, around two thirds of all prisoners have substance use disorders–including both drugs and alcohol. For many of these people, their crimes were related to their substance use disorder in that they:

Currently, while many prisons offer some treatment programs, most do not have the trained staff to provide treatment to all who need it and few programs use up-to-date methods. By the latest estimates, only about one in ten people in prison who have a substance use disorder have received treatment. They were then introduced to a proposal that has been put forward in Congress to, “provide additional funds to cities and states that want to expand and improve the treatment programs in their prisons.” Arguments The pro argument was found convincing by a large and bipartisan majority, while the con argument was not found convincing by any majority. Final Recommendation Asked for their final recommendation, 74% favored the proposal, including 61% of Republicans, 89% of Democrats and 71% of independents. |

|

Survey: PPC, June 2022 Respondents were asked whether they favor the following: Provide funds to cities and states that want to set up or expand programs that:

A bipartisan majority of 74% favored the proposal, including 58% of Republicans, 90% of Democrats and 71% of independents. More Details Briefing Some cities have set up programs that enable and encourage police officers, when they interact with a person who has committed a minor non-violent crime as a result of their substance use disorder, to get them into a treatment program rather than charge them with a crime. This is called a “diversion” program. Respondents were introduced to this idea, as follows: As you may know, when a law enforcement officer encounters someone committing a minor non-violent offense, such as possessing a small amount of drugs, loitering, or disturbing the peace, they have various options. They can choose to arrest them, give them a warning, or let them go. There is an additional option being used in some cities: if law enforcement officers perceive that a non-violent offender has a substance use disorder, rather than charging them with a crime, require them to enter a treatment program and give them information about available programs. If the person refuses, they may be charged. They were then presented the following proposal: In Congress, there is a proposal to provide funds to allow cities and states to set up or expand such programs. These programs would:

Arguments The argument in favor was found convincing by a large majority, overall and among Republicans and Democrats. The argument against was found convincing by just under half, but a large majority of Republicans and half of independents also found it convincing. Final Recommendation Respondents were then presented the proposal again: Provide funds to cities and states that want to set up or expand programs that:

Asked for their final recommendation, 74% favored the proposal, including 58% of Republicans, 90% of Democrats and 71% of independents. |

|

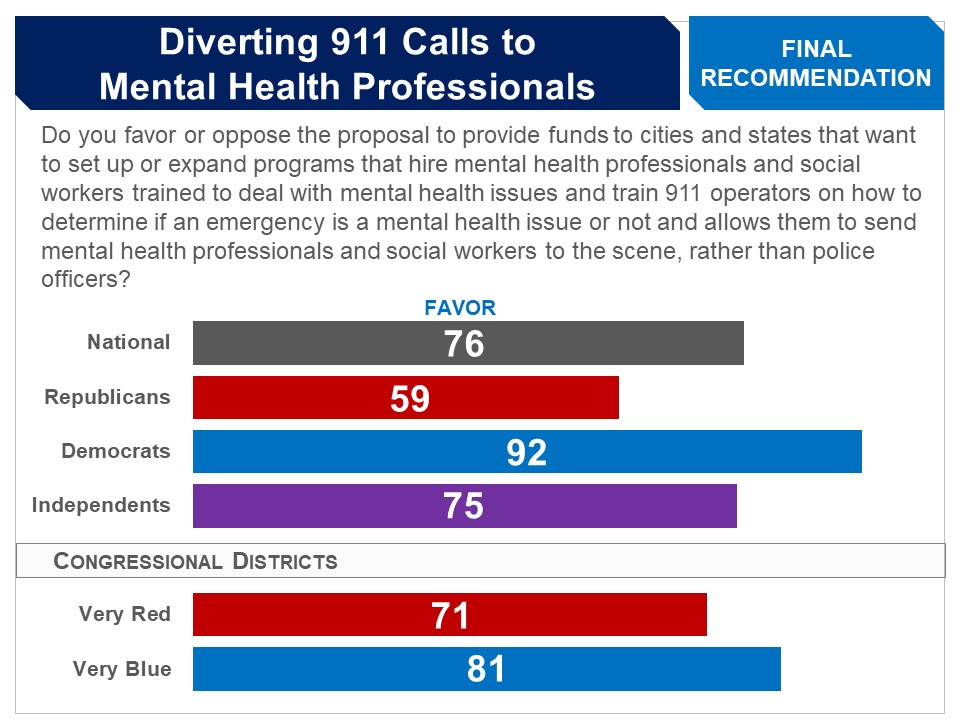

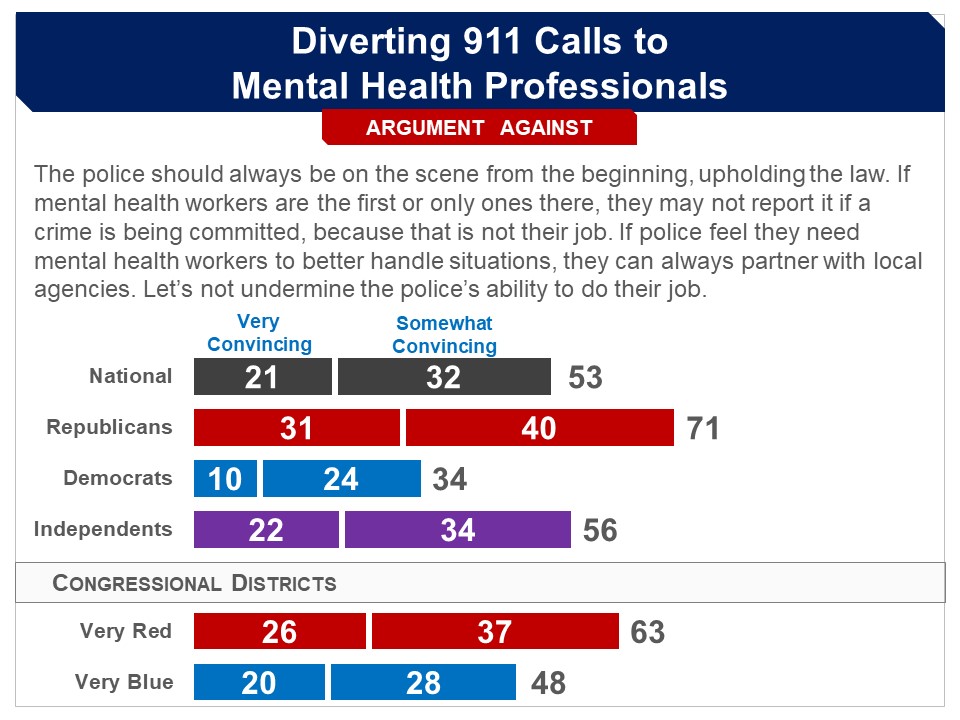

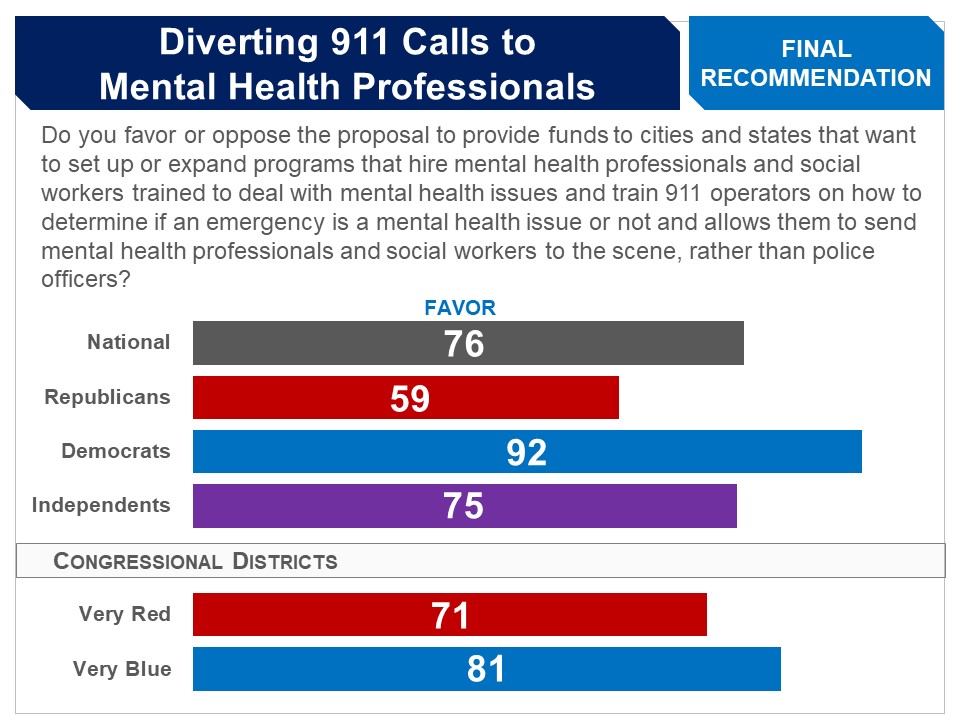

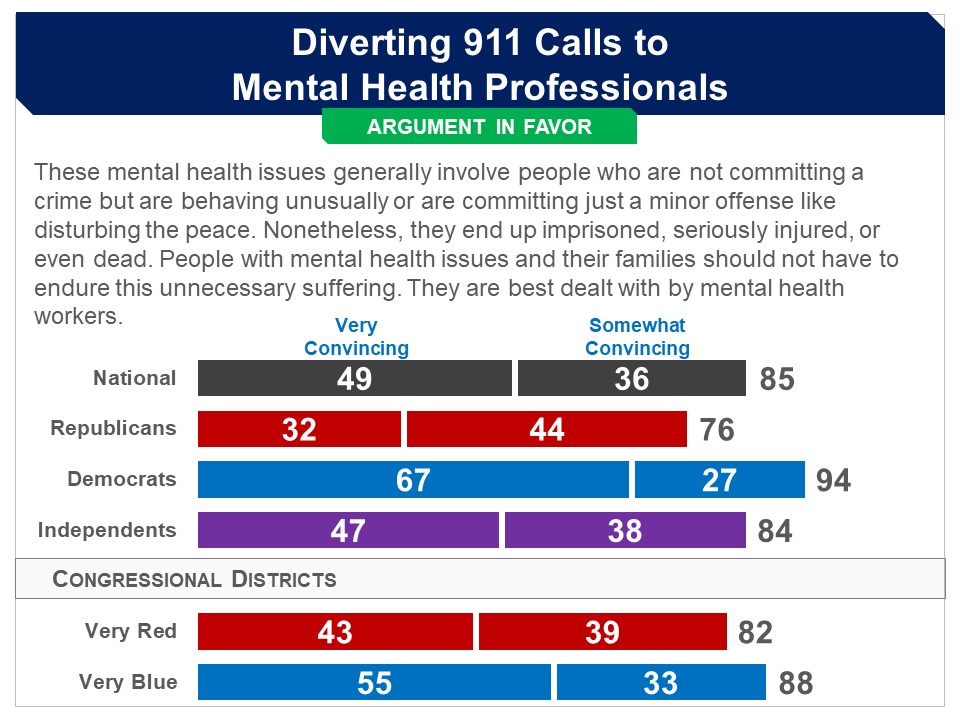

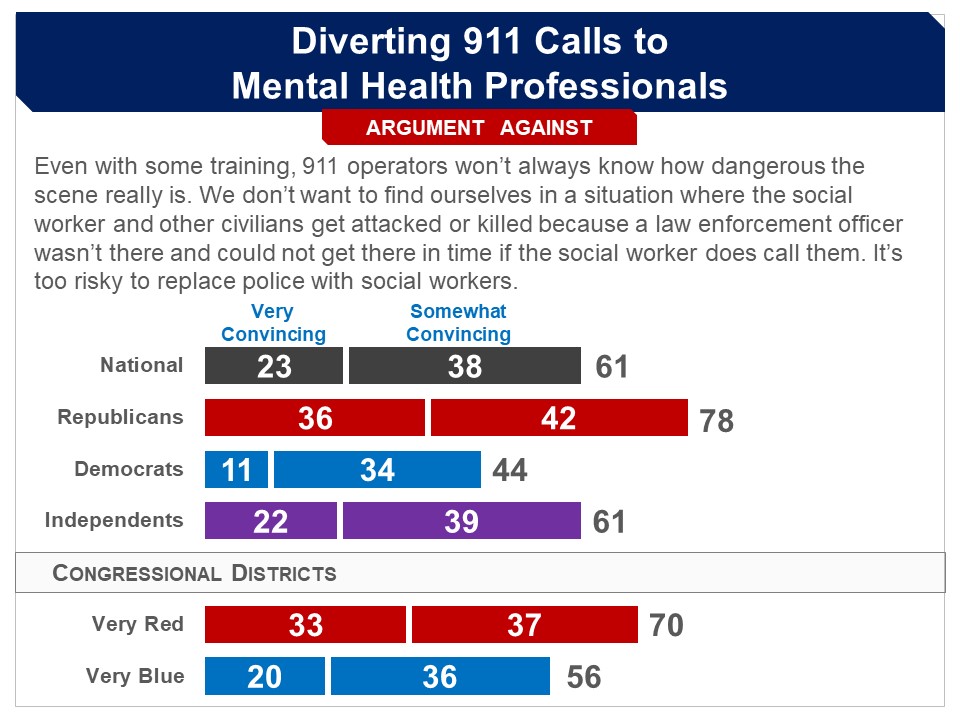

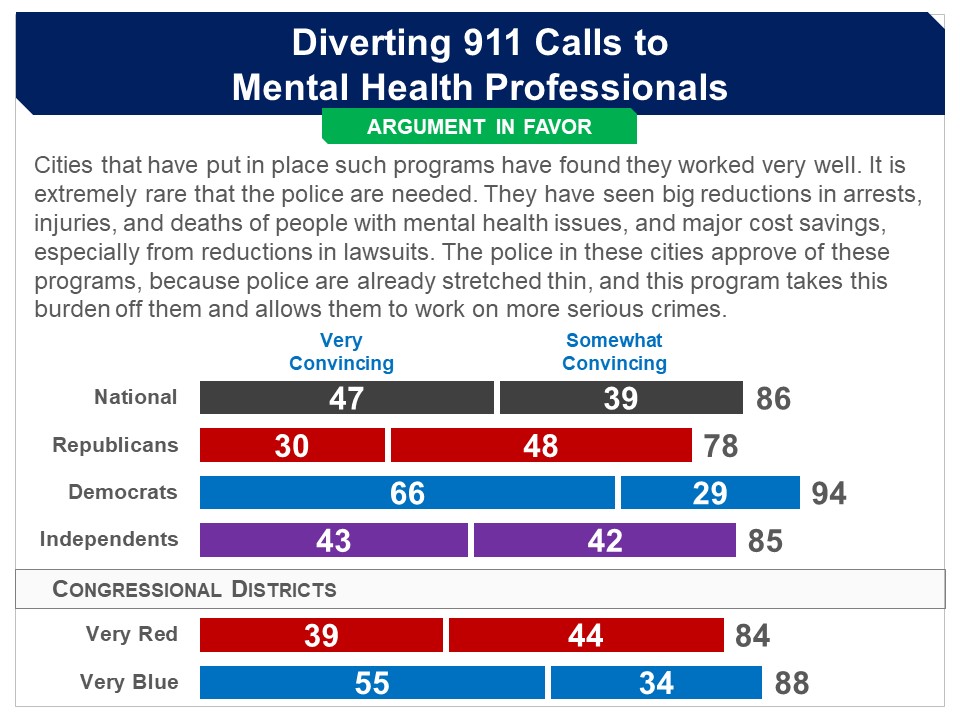

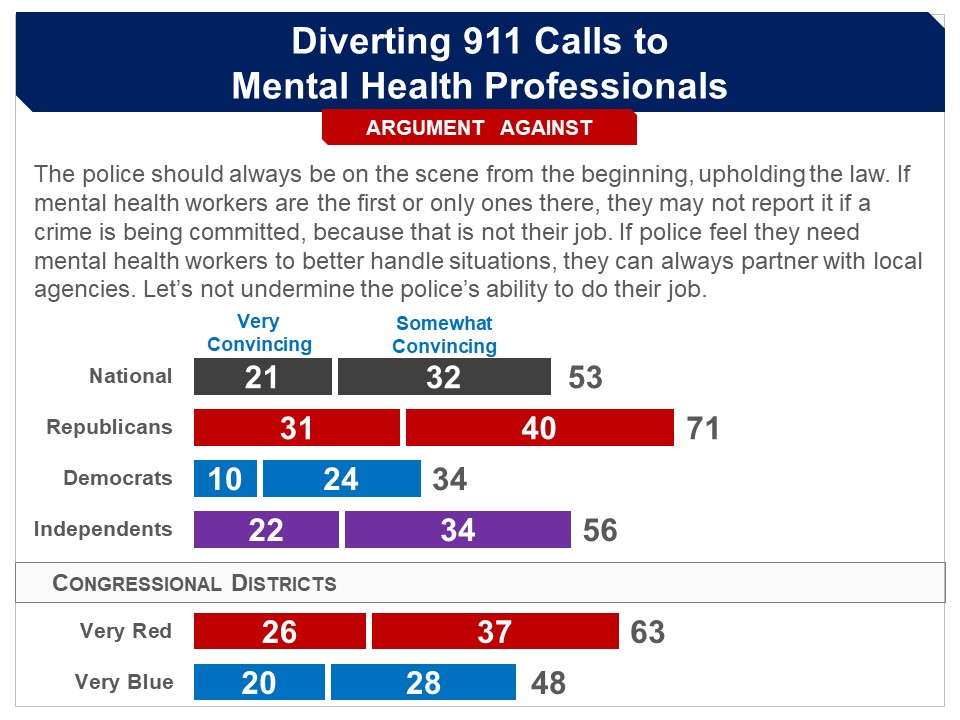

Survey: PPC, June 2022 Respondents were asked whether they favor the following: Provide funds to cities and states that want to set up or expand programs that:

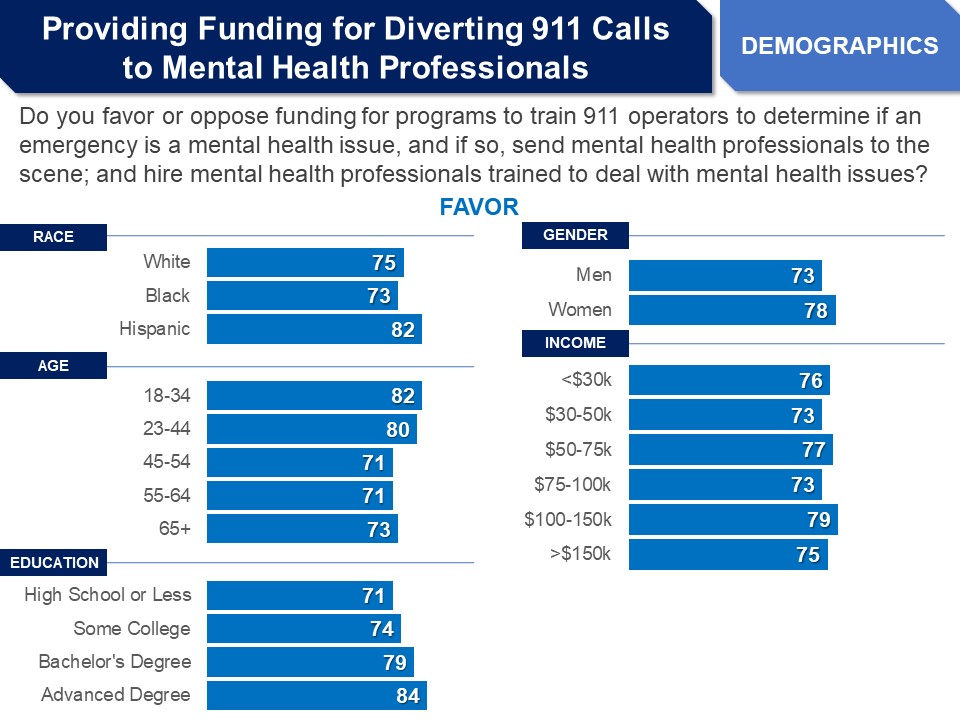

A bipartisan majority of 76% favored this proposal, including 59% of Republicans, 92% of Democrats and 75% of independents. Demographics

More Details Briefing Respondents were presented background information on interactions between police officers and those with mental health issues, as follows: people will often call 911 because they are concerned that a person:

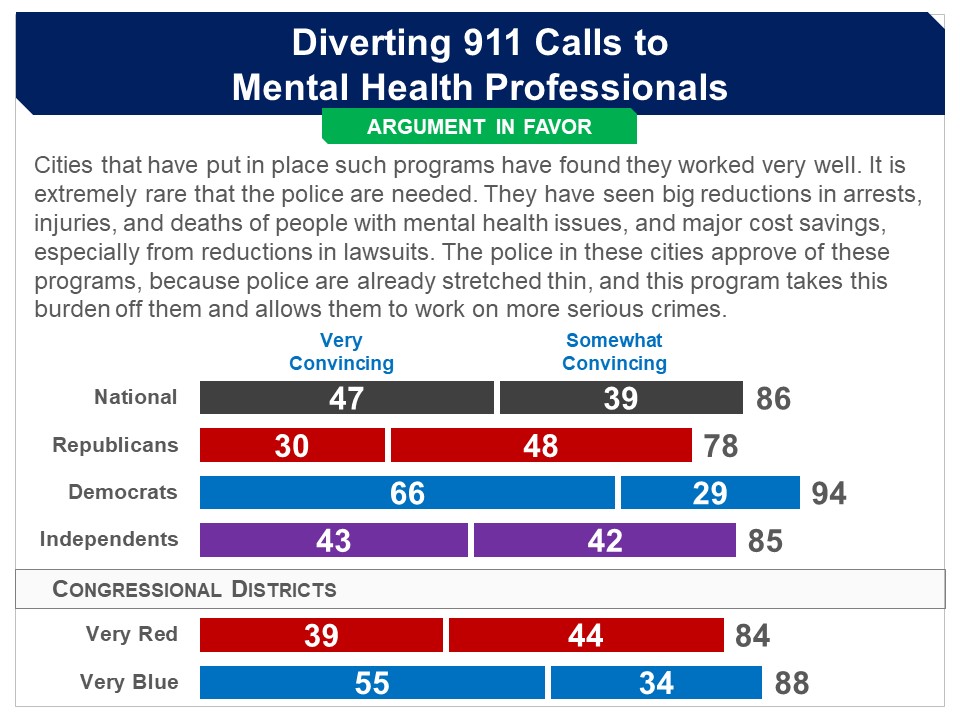

In nearly all cities, the 911 operator sends law enforcement to the scene. Many police officers, however, are not trained to deal with people with mental health issues. Thus, when officers encounter such people, they sometimes do not understand what is occurring and may act in ways that provoke a reaction in the person. Police officers may then try to arrest the person which has led to escalation resulting in injury or even death. They were then introduced to programs that have been set up which send mental health professionals to such scenes first, rather than police officers: A few cities (including in Texas, Oregon and other states) have established programs that deal with people having mental health issues by using professionals trained to deal with them rather than police officers. More specifically the programs :

The goal of these programs is to use as little force as possible and to get the person having a mental health issue back home or into a hospital, and into a mental health treatment program if they are not already in one, rather than have them arrested and put in jail. In some cases, these professionals can bring a law enforcement officer if they feel it is needed or call one if the situation does escalate. Evaluation of these programs have found that they have resulted in reductions in the use of force, injuries, arrests, and incarcerations. They have also resulted in reductions of costs related to imprisonment and lawsuits over the use of excessive force. Respondents were then told that there is a proposal to, “provide funds to cities and states that want to set up such programs or want to expand existing programs.” Arguments The argument in favor was found convincing by a very large and bipartisan majority. The argument against was found convincing by a smaller but still substantial majority, but less than half of Democrats. Final Recommendation In the end, respondents were presented a summarized version of the proposal: Provide funds to cities and states that want to set up or expand programs that:

A bipartisan majority of 76% favored this proposal, including 59% of Republicans, 92% of Democrats and 75% of independents. |

Related Standard Polls

Related Standard Polls

Pre-Deliberation Poll

Pre-Deliberation Poll